Why This Economic Cycle Is Different

I recently wrote a brief history of credit cards in America.

Here is a brief summary of consumer spending in the current period:

Consumer credit first started in the 20s as Americans wanted all the new household items on the market.

The Great Depression crushed the stock market, crushed the economy, crushed the consumer and turned a generation of households into penny pinchers who were too afraid to spend money.

After World War II everything changed as consumer debt exploded from the creation of suburban America and the middle class.

Credit cards exploded onto the scene in the 1960s taking more money. Then the inflation of the 1970s hit and debt was actually a commodity in some ways because purchasing power was being depleted very quickly.

By the 1980s and 1990s, consumerism and credit had replaced the family mind and bank account. We like to spend money in this country and we are very good at it.

In many ways, the Great Financial Crisis was caused by debt accumulated over the past 30 years or so. That financial crisis continued for years.

But after the 2008 disaster, families (collectively) learned their lesson. No more cash withdrawals to take vacations or buy more houses. No more NINJA loans.1 No more adjustable rate loans. Families adjusted their balance sheets.

Yes the debt continued to rise but that will happen if the economy grows. The good news is that debt has increased at a very low rate.

Look at the change in household assets and debt over the decade going back to 1989:

From 1989-1999, household goods and debt grew at the same pace, both doubling in size. Then from 1999-2009, debt grew faster than assets. Two recessions, a housing bubble and two stock market crashes had a lot to do with that but clearly this was wrong.

Now look at what happened from 2009-2019 – assets grew faster and debt growth slowed significantly. The same thing happened in this decade. Asset growth outpaces debt growth.

That’s why the house rent is so high.

Matthew Klein at The Overshoot tries to put this decade’s wealth gain into context:

In other words, $66 billion in net wealth has been added in less than six years, which is equivalent to tripling all personal consumption expenditures (PCE) by 2025.

Obviously, booming real estate and the stock market have a lot to do with these gains.

The housing market perfectly encapsulates the difference between asset and debt growth in this cycle and why this time is different.

In 2009, the total value of the real estate market in America was estimated at $19 trillion. Total mortgage debt outstanding was just over $10 trillion.

Today the housing market is worth $48 trillion and the outstanding mortgage debt is $13.6 trillion. Mortgage debt makes up about 70% of total consumer debt.

To be honest, this has been a once in a lifetime housing price boom. Mortgage rates were at generation lows. This will not last forever. But this is one of the reasons why households are in much better shape from a balance sheet perspective than in previous cycles.

There is a case to be made that domestic balance sheets have never been in better shape than they are today.

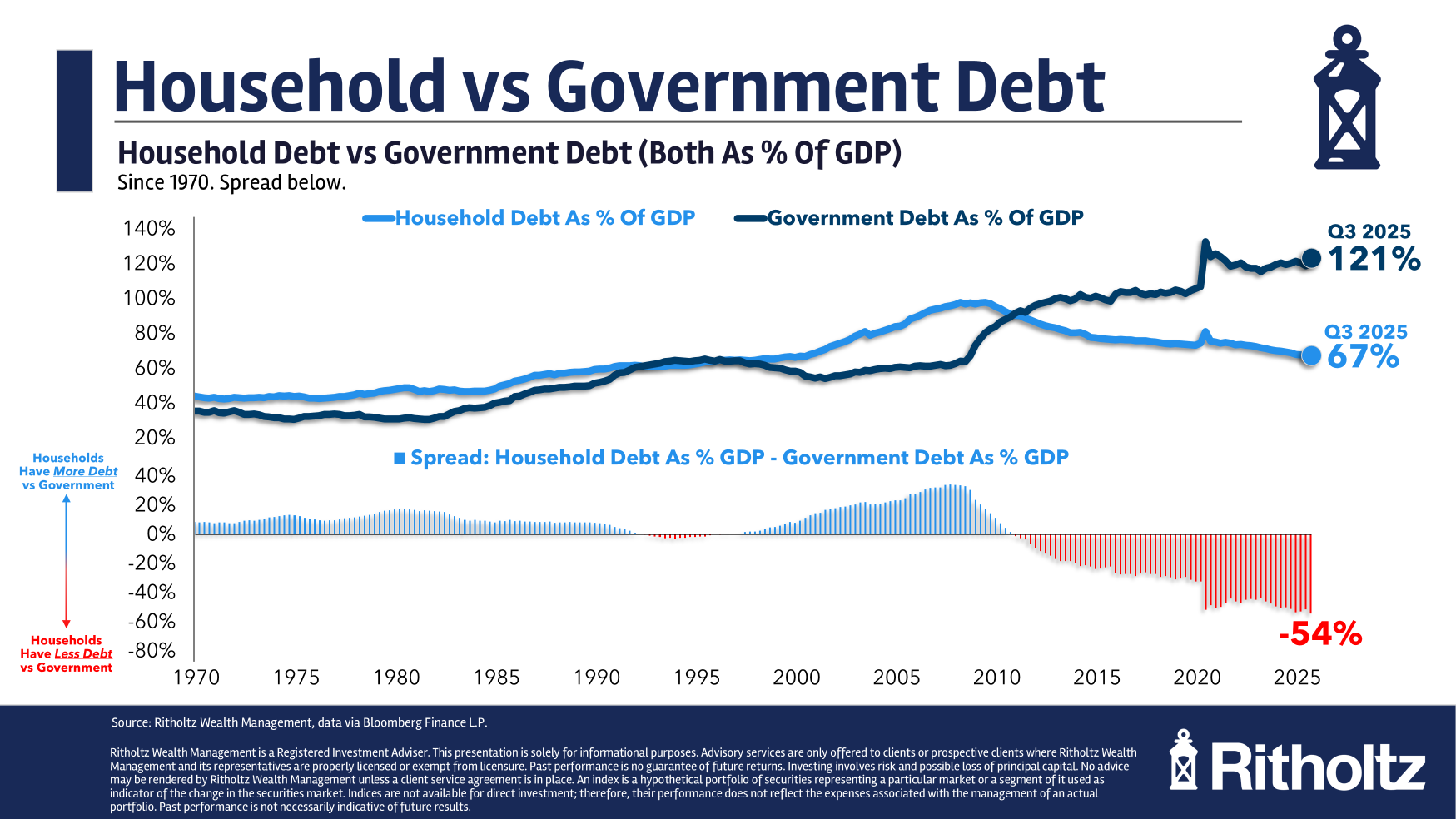

The argument is that domestic balance sheets are in good shape because government debt is unmanageable. Here’s a look at household and federal debt-to-GDP going back to 1970:

As households repaired their balance sheets from the 2008 financial crisis, the US government borrowed more money than ever before. Government debt-to-GDP increased significantly while household debt-to-GDP decreased significantly.

The level of government debt is a topic for another time, but I would very much like to have an institution with the power to print the world’s reserve currency and tax its citizens who take on more debt than households.

Household balance sheets will not always be this clean. Sometimes this cycle will reverse.

The economy will go into recession. Commodity prices will fall. Credit will rise as consumers borrow money to stay afloat.

But the good news is that families have never been in a better position to weather a hurricane. Borrowing capacity is now much higher because credit growth has slowed.

This is not like the previous cycles.

This time is really different.

Further reading:

Why Are Credit Card Rates So High?

1No salary, no job, no mortgage was actually a factor in the housing bubble.