The economy of a 50-year loan

A student asks:

Ben has been hitting on people who pay their mortgages early. Does that mean you are a fan of the 50 year long mortgage

The US Housing Authority says the government is looking at 50-year mortgages:

Will it ever happen?

I don’t know but that won’t protect me from running the numbers.

The initial reaction to the proposal was negative across the board. Personal finance defies this idea.

Let’s look at the numbers to see why.

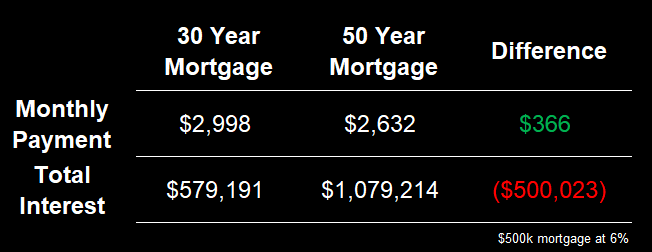

I like round numbers so let’s look at a $500,000 mortgage with 6 percent interest over 30 to 50 years:

The monthly payment is slightly lower but the lifetime interest paid is way higher.

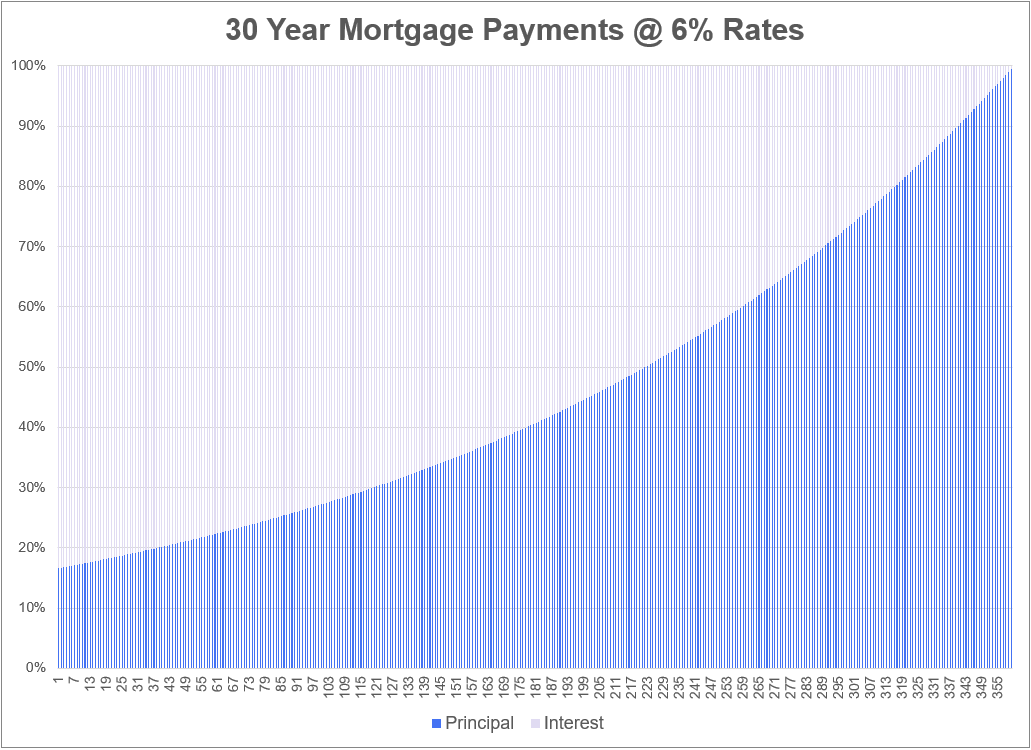

Now let’s take a look at the monthly payment profile to see why a 50-year mortgage isn’t great in terms of construction.

This is the breakdown of the payment between principal and interest on a 6-year mortgage at 6%:

You initially pay 83% of your payment in interest charges and 17% in principal payments. This is how electricity works with loans for this.

Now let’s look at a 50-year loan:

Basically your down payment – 95% – covers interest charges. It takes a long time to make a big dent in your ass.

After 10 years, this is the amount of equity you will have in the home for each term of the loan:

- Year 30: $81,571

- Age 50: $21,636

This is the biggest problem people have with a 50 year loan. You don’t really build any equity without growing home values.

And this example uses the same interest rate for both periods. Currently 30-year mortgage rates are about 0.5% higher than 15-year mortgages:

You would think that a 50 year loan would have a higher rate than a 30 year. If there was a second point spread between the 30-year and 50-year mortgage rates, you would only save $217/month ($2,998 vs. $2,781) in my simple example.

It doesn’t go well with the needle in terms of money supply.

That takes Glass-half-ansurang.

Now let me play Devil’s advocate.

No one lives in a house for 50 years. The average homeowner in America is somewhere between 10 and 12 years old. Therefore, you will have to look for a 50-year loan such as a mortgage loan that allows you to lock in the payment and remodel tile.

That’s not a bad way to look at this but it’s done well. If the idea is to fix the housing market and make it more affordable for young people to buy, that’s not the answer. This is like a band-aid on a machete wound.

If we’re just going to throw some ideas against the wall to see what mine is:

Why don’t we offer any first time home buyer a 3% down payment?

It’s not your fault if you missed out on generation-low interest rates in the early 2020s because of bad timing in your life stage. Low bond prices will have the greatest impact on pre-50 year old funds.

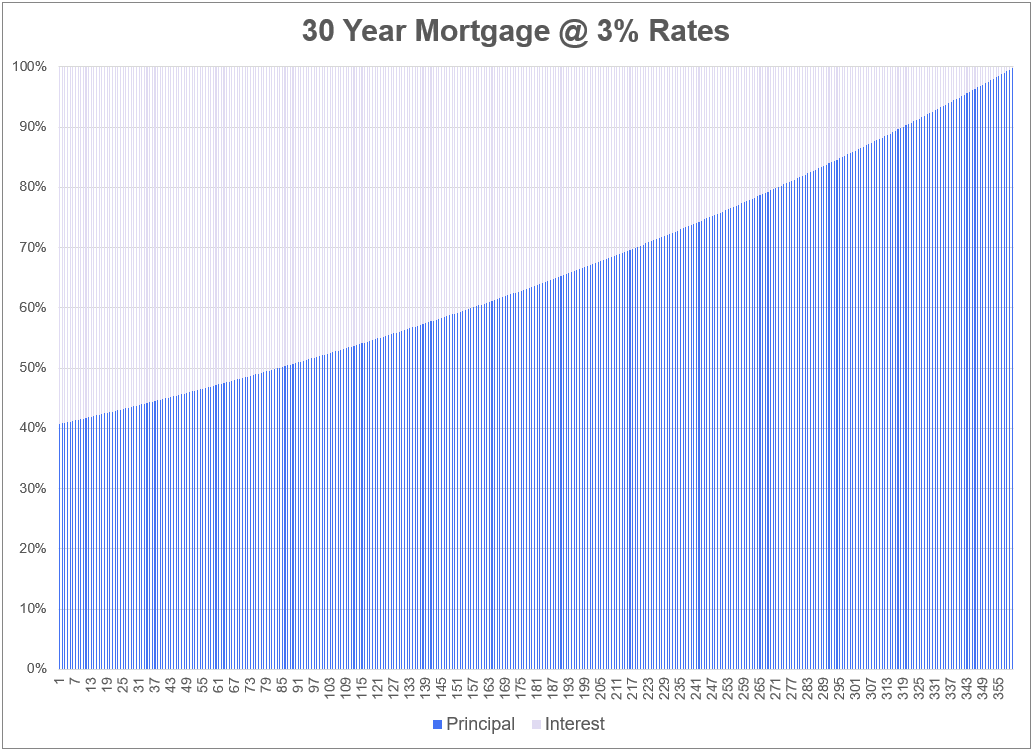

Here’s the myth of a 6% and 3% mortgage on a $500,000 loan over 30 years:

The monthly payment and the total interest paid are low.

Now look at the Payment Profile:

That’s why 3% mortgage rates are probably one of the best home financing assets ever seen. You get the highest percentage of your payment that will go to the PAITHERDODE for a high rate or long term loan.

The government, presumably Freddie and Fannie, would have to repay the loan. Or maybe the Fed could buy mortgage-backed bonds to bring down the prices of those bonds.

I know it doesn’t seem right for the government to get into the Housing Market but this is exactly the way it was for the middle class in the 1950’s. The government guaranteed loans for home builders to put the risk on their shoulders. They offer VA property loans for soldiers coming home from WWII. They encourage the construction of more homes.

Obviously, building more homes would be a more desirable solution for everyone.

Increasing home delivery will relieve a lot of pressure on consumers. The federal government should encourage local governments to change their building restrictions to facilitate the construction of more houses without unnecessary red tape. If we are going to postpone, the most important area is housing.

Financial Engineering is easier than building in the physical world but building many houses actually works.

Until then it will have to be creative unless we want all our young people to rise up because they can’t buy a house.

We’ve broken this question down with the latest version of the combined query:

https://www.youtube.com/watch?v=svi2jz-vlsk

Jonathan Novy of Ritholtz Chinago joined me on the show this week to discuss questions about the Kyle Busch Insurance Scandal, retirement risk succession, asset allocation decisions and learning vs. Getting ahead of your financial deck.

Further reading:

Housing Market NOBility