Unit Investment Trusts (UIT) vs. ETFs

vs. ETFs")

Some investors have discovered that their investment is not a mutual fund—not a traditional personal fund or Exchange Traded Fund (ETF). Rather, it is a Unit Investment Trust (UIT). And they begin to wonder what a UIT is, how it differs from an ETF, and whether that difference really matters in their financial life.

Today, let’s talk about UITs.

What is a Unit Investment Trust (UIT)?

A UIT (though better than a UTI) is a type of investment vehicle that holds a fixed portfolio of securities, such as stocks and bonds, and sells “redeemable units” (ie, shares) to investors. Unlike a mutual fund, a UIT is a static portfolio that is held until a specific “cut-off date” that cannot be continuously managed. Therefore, its holding does not change.

A UIT is created by an investor who selects and purchases a portfolio of securities based on a specific investment objective; then, they raise money for investors by selling them affordable units. Then, it is simply held until liquidation, when the securities are sold and returned to investors. Since no management takes place, there are no ongoing management fees (although there is often a creation and performance fee). It is usually possible to sell the shares back to the sponsor before the liquidation date.

How Is a Unit Investment Trust Different from a Closed-End Fund?

Most mutual funds are open-ended, meaning they get bigger and smaller as money is contributed or spent in the fund, and the shares always trade at their Net Asset Value (NAV). However, some mutual funds are closed. They are neither big nor small and often sell at a premium or discount to NAV due to their illiquidity.

A UIT sure sounds a lot like a closed-end fund (CEF), doesn’t it? However, there are two important differences:

- UITs have fixed, unmanaged portfolios. CEFs are actively managed.

- UITs have an expiration date. CEFs trade indefinitely on an exchange.

More info here:

Separately Managed Accounts (SMAs): Are They Worth Your Money?

Composite ETFs – What You Need to Know

What are the Advantages of Unit Investment Trust over ETF?

UITs have some advantages over traditional open-end mutual funds, CEFs, and ETFs.

- No active management: Active management has generally been shown to be harmful to investors over the long term. While many open-ended mutual funds and ETFs are passively regulated, again, many of them are not. All UITs are passively managed.

- Low cost: Since there are no managers, there is no management fee, reducing costs. Those savings can be passed on to investors, although, to me, some operating costs still seem very similar to management fees.

- There are no “fire sales” in turbulent markets: When investors want to exit open-ended mutual funds after a major market decline, the manager is often forced to sell the securities at a loss. This is not the case with CEFs, UITs, and ETFs, as these may not be redeemable (CEFs and UITs) or stocks with a different creation/destruction process (ETFs).

- Ability to buy below NAV: Sometimes, CEFs and UITs can be bought at a discount to NAV. That is never available with traditional mutual funds (which always trade at NAV) or ETFs (where Authorized Participants will immediately settle any differences in NAV to eliminate discounts and premiums).

- Being able to “install:” UITs can use leverage (borrowed capital) in ways that mutual funds have difficulty doing. UITs can invest in loans alongside their capital.

- Dividend smoothing: Mutual funds and ETFs must distribute all of their dividends to investors. UITs and CEFs can hold up to 15% of it and create a cash reserve. That reserve can be used to accelerate dividend payments over time, making the income more visible.

What are the Disadvantages of Unit Investment Trust?

Naturally, UITs have their downsides, too. There is a reason that more money is invested in traditional mutual funds and especially ETFs these days than in mutual funds and UITs.

- Lack of flexibility: The main disadvantage stems from the fixed, unmanaged portfolio structure. The fund cannot react well to market changes. It doesn’t measure up.

- Lack of liquidity: You may sell the units back to the sponsor in the secondary market, but you may also be locked into the investment until you are terminated or face significant closing costs. And since UITs often trade at a discount to NAV, there is less wind when paying NAV to get into an investment.

- Advance and ongoing payments: UITs are often sold with loads (commissions) by brokers. They can also charge large operating fees despite the lack of effective management. This encourages brokers to recommend moving from one UIT to another, generating a new commission.

- Termination is a taxable event: You no longer have control over when you will liquidate your investment. When the UIT expires, you will receive (hopefully) large gains and have to pay taxes on them.

- Lack of diversity: UITs are sometimes not very diversified, and focus on a small market sector.

More info here:

Should Physicians Consider Angel Investment?

Emotions Behind Short Term Trading

What UITs Have I Heard About?

Some investors are surprised to learn that they have a UIT instead of an ETF. Here are some that are commonly owned.

CHECK

That’s right, SPY (SPDR S&P 500 ETF Trust) isn’t actually an ETF. UIT. It would be interesting to compare SPY with the Vanguard 500 Index ETF (VOO). SPY has a high trading volume and a slightly lower bid-ask spread, so it may be preferred by high-frequency traders. But that ETF structure gives VOO an edge over all other options that apply to long-term investors.

SPY may be useful for short-term trading due to its high volume and tight bid-ask spread, but VOO is the best long-term holding due to its low cost, better integration, and tax efficiency for those investing in taxable accounts.

QQQ

QQQ (Invesco QQQ Trust Series I) is also a UIT, not an ETF. I recently received an email from a WCIer with the subject:

“This may be too dense for WCI, but anyway I thought you might know the answer. I, for unusual reasons related to the investment gifted from the parents, hold some shares available (QQQ). The shareholders are currently being asked to vote on the conversion from UIT to ETF format. I have been googling, but it seems a little opaque. 0.20 ER can always be nice But I would accept your explanation of the difference and thoughts about the issue at hand and in general.

An ETF structure is tax efficient over the long term and often cheaper than a UIT structure. UITs have been around for a long time. The first was in the UK in 1931, which was created as a result of the Great Depression and the associated stock market crash. The first ETF was not created until 1990 in Canada. The first to be traded on a US exchange is usually listed as SPY—which, as we know, is not technically an ETF as we define it today. The first Vanguard ETF was VTI (2001), and the first iShares (now Blackrock, but previously Morgan Stanley and Barclays) ETFs were launched in 1996 (bonds in 2002). Of note, QQQM is basically the same thing as QQQ, except it’s a true ETF, not a UIT.

DIA

Why anyone would want an index fund/ETF that tracks the Dow Jones is beyond me, but apparently, back in the 1990s, some people did. DIA is still around, and you may have heard of it.

If My UIT Wants to Convert to an ETF, Should I Vote Yes?

Yes. According to this Business Insider article from 2014, there were only 8 “ETFs” (of the >8,500 ETFs currently in existence) that were actually UITs at the time:

- CHECK

- QQQ

- MDY

- DIA

- ADRA

- ADRD

- ADRE

- ADRU

QQQ switched to a true ETF structure in December 2025 (lowering ER from 0.20 to 0.18), and I suspect others are not far behind. I see little benefit in the UIT structure compared to the ETF structure.

More info here:

My Favorite Mutual Fund

How Do You Measure and Compare Mutual Funds and Mutual Funds?

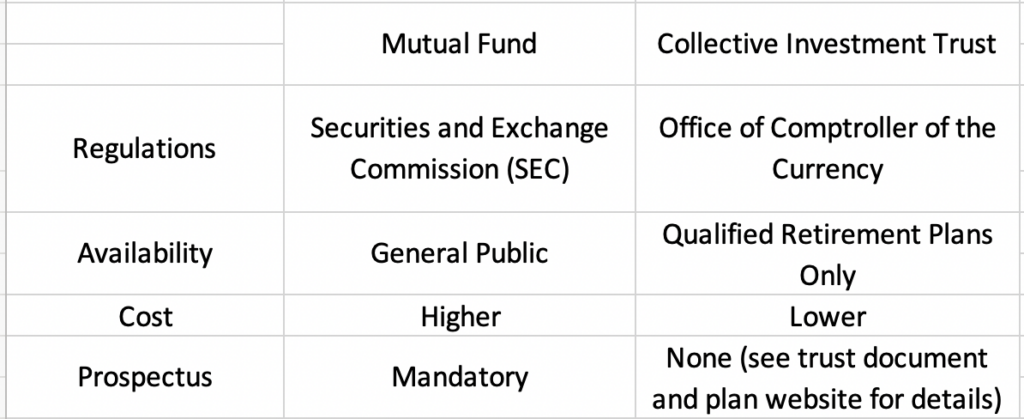

Is a Unit Investment Trust the Same as a Collective Investment Trust?

No. Two of the three words were the same, but since the third is different, it has a completely different meaning. While the UIT is historically an oddball with little benefit over an ETF and while only a few still exist, the Collective Investment Trust (CIT) has become more common and more common in 401(k)s across the country. There are actually more than eight of them out there. A CIT is a mutual fund alternative that is only available within qualified retirement plans, such as your 401(k). It’s best to just think of it as the same thing as a mutual fund, but there are a few small differences, which aren’t necessarily bad.

Bottom line, CITs are sometimes placed in a 401(k) instead of mutual funds because they are less expensive due to lower administrative costs. Most of them are index funds or balanced lifestyle funds, usually a good thing for 401(k) participants. However, because they don’t have ticker symbols like mutual funds and stocks, CITs can be a bit harder to research online (like Morningstar and other similar services). Often, you will need to find and review information provided by Human Resources at your company or 401(k) provider to learn more about investments.

WHAT DO YOU THINK? Would you vote to convert UIT to ETF? Why or why not? Does your 401(k) use funds or CITs?