Should You Use a ‘Safe’ Withdrawal Rate?

It is widely accepted that the “safe” withdrawal rate is 4%, which means that if you retire with $3 million, you can spend about $120,000 a year, adjusted each year for inflation, and expect your money to last 30 years with a very high level of confidence. Although there are no guarantees in life, this is considered safe. This data was first shown to the public through the Trinity Study back in the 1990s. If you have never seen this table, spend some time with it to understand this discussion and others like it.

Using historical data and a 50/50 portfolio, a theoretical retirement using 4% (adjusted for inflation each year) defaulted only 4% of the time. At 5% of spend, that rises to a failure rate of 1/3 of the time, and at 6%, that rises to 1/2 of the time. That’s why 4% is considered a safe withdrawal rate (SWR) and 5%-6%, roughly the 8% advisors were telling their clients in the 1990s, is a dangerous withdrawal rate.

But what is that danger? I mean, most retirees don’t know anything about this study or this table. They don’t even count their withdrawal rates, and most of them don’t run out of money. What happened? Perhaps we need to understand that in order to respond rationally to conservatives recommending a 3.5% withdrawal rate and extremes recommending a 2.5% withdrawal rate. Even if people argue about a difficult withdrawal strategy that requires the use of constant corrections, calculators, guidelines, and watch lines.

Real Risk of Bankruptcy

Let’s see if we can calculate the true risk of bankruptcy in retirement for a retired multi-millionaire physician. Let’s say these docs retire with $5 million, and are willing to take reasonable risks in their lives. What exactly has to happen for them to go bankrupt?

Five things, really. And all must come to pass; not just one of them.

#1 They Have to Retract More than the SWR Can Suggest

We can argue if that’s 4%, 3.75%, 3.5%, whatever. But if the probability of failure is 0% by all possible calculations (like any number less than 3%), they will never run out of money, no matter what.

#2 They Should Go On A Bad Return Series

No one will run out of money—even with a 7% withdrawal rate—if they get a good sequence of returns in retirement. For a 75/25 portfolio, a 7% SWR worked for 30 years 45% of the time. Those people who retire in 2010 will do well.

#3 They Should Live Long Enough

The Trinity study has used 30 years in vain. But look how much better all those numbers look in 15-20 years, the actual life expectancy of a 63-68 year old retiree. At 75/25, a 6% withdrawal rate worked 97% of the time for 15 years. Always remember the lesson of the Rich, Broke, or Dead chart—where green is rich, red is broke, and black is dead.

More people die prematurely than are violated.

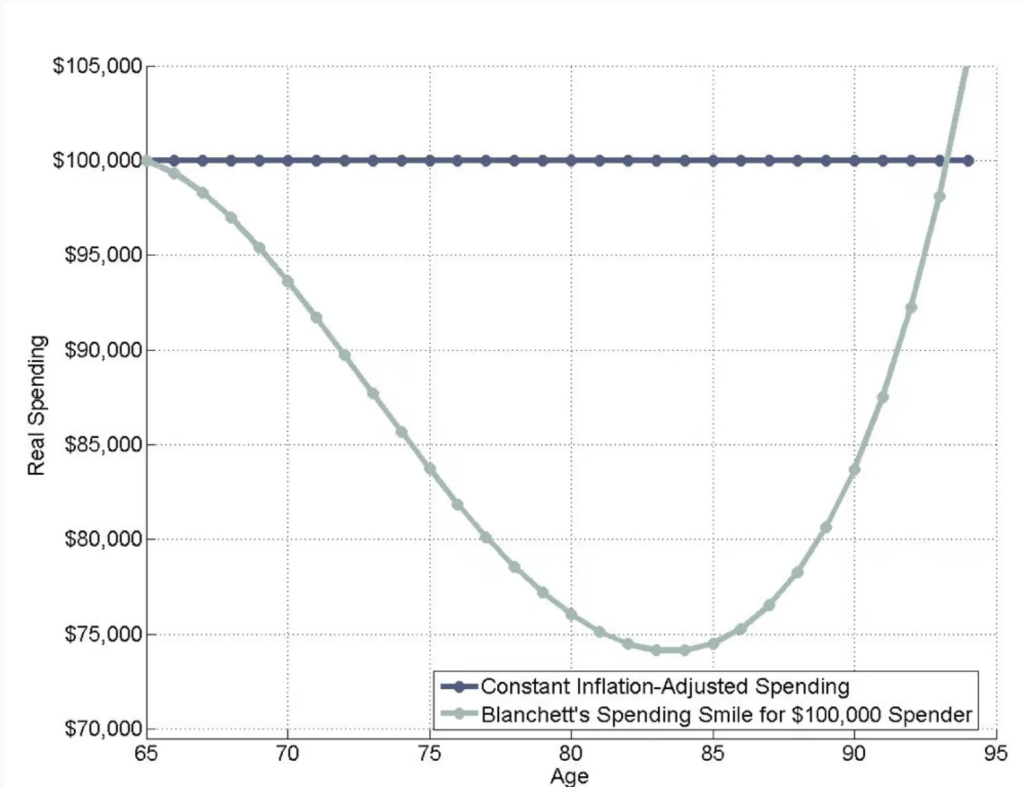

#4 They Should Continue to Spend the Same Amount During the Declining Years as They Were in the Declining Years

Retirement income is often referred to as a smile. David Blanchett drew it like this in 2014:

Blanchett thinks that spending has dropped by 20% or more during the years of slow travel. I don’t know if that’s accurate, but for most people, it slows down after the initial excitement of traveling and having fun turns into too much of a burden.

#5 They Can’t Make Any Changes If All of the Above Really Happens

Flexibility in how you spend your retirement income is very important. You might be surprised how flexible you have to be to use an aggressive withdrawal rate (Big ERN suggests it could require up to a 50% cost reduction), but if your spending habits are more flexible, that’s an option. Of course, any amount of flexibility can help reduce the risk of running out of money, and most multi-millionaire retirees have little flexibility in their budgets.

More info here:

How Flexible Can You Be in Retirement?

Comparing Portfolio Withdrawal Strategies for Retirement

Do the Math

Now, let’s assign some probability to these numbers and do some math. Let’s use a 5% withdrawal rate, which is obviously above the “safe” withdrawal rate. And suppose a bad sequence of returns (basically, the economy tanks just as you retire or soon after) occurs. For a 75/25 portfolio, that’s 18% (over 30 years). Now, let’s say you are 65 years old and single. What is the probability that you will live to 30 years? If you are male, it is 5%. Let’s multiply by 18% x 5%. That’s 0.9%. That seems pretty low, no? Even if you use the number of 20 years (5% chance of bankruptcy) and multiply that by the chance of you still being alive after 20 years (37%), you end up with 1.85%. Now drop that 0.9%-1.8% on the other two factors, spending less in the slower years and making some adjustments as you go. I don’t know how to do the math for that, but let’s say you drop it to 0.5%. That’s 1 in 200.

Are you willing to take such a risk in your life? Of course I am. Of course, most people who start with a 5% withdrawal rate will obviously NOT run out of money.

More info here:

Here’s How Much The Man Who Invented The 4% Rule Is Actually Spending In Retirement (Spoiler: It’s More Than 4%)

How to Use Your Nest Egg — Possibilities versus safety first

How WCI Students Live, Worry, and Cash Out in Retirement

Should You Use a Safe Withdrawal Rate?

Should you use a safe withdrawal rate if you can be fine without it? I think you should still do it, especially if you’re retiring before your 60s, but I don’t think you need to do anything more than that. And you certainly don’t have to listen to anyone out there telling you that if you withdraw more than 2.836%, you will be eating Alpo. And once you’re 88 years old, 4% is no longer a “safe” number—6%, 8%, or more is fine at that point. Even your RMD for those years is 7.3%. Trees do not grow to the sky, and you are not immortal.

WHAT DO YOU THINK? Would you be willing to risk a withdrawal rate of more than 4%? Why or why not?