Animal Spirits: Gold’s 1987 Moment

Today’s Animal Spirits is brought to you by Nuveen and ClearBridge Investments:

Today’s show is sponsored by ClearBridge Investments. International and emerging market stocks outperformed the US in 2025. At ClearBridge, we believe this momentum can continue. Find out more at

Today’s show is sponsored by ClearBridge Investments. International and emerging market stocks outperformed the US in 2025. At ClearBridge, we believe this momentum can continue. Find out more at

On today’s show, we discuss:

Listen here:

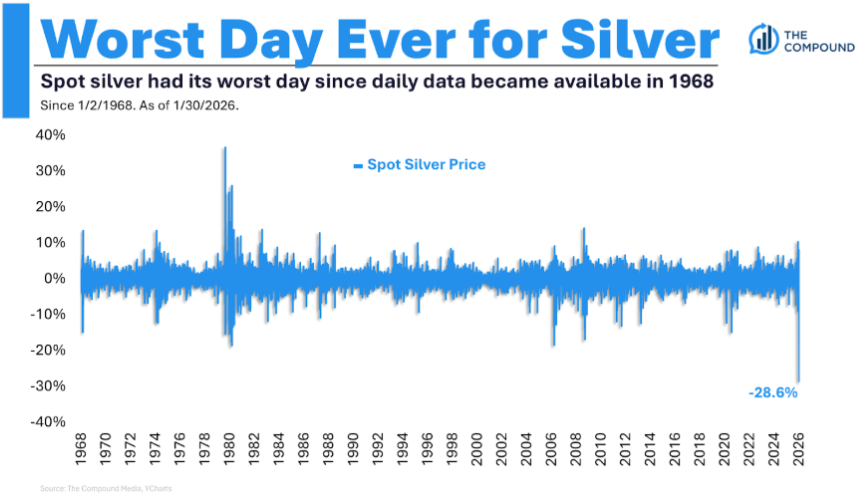

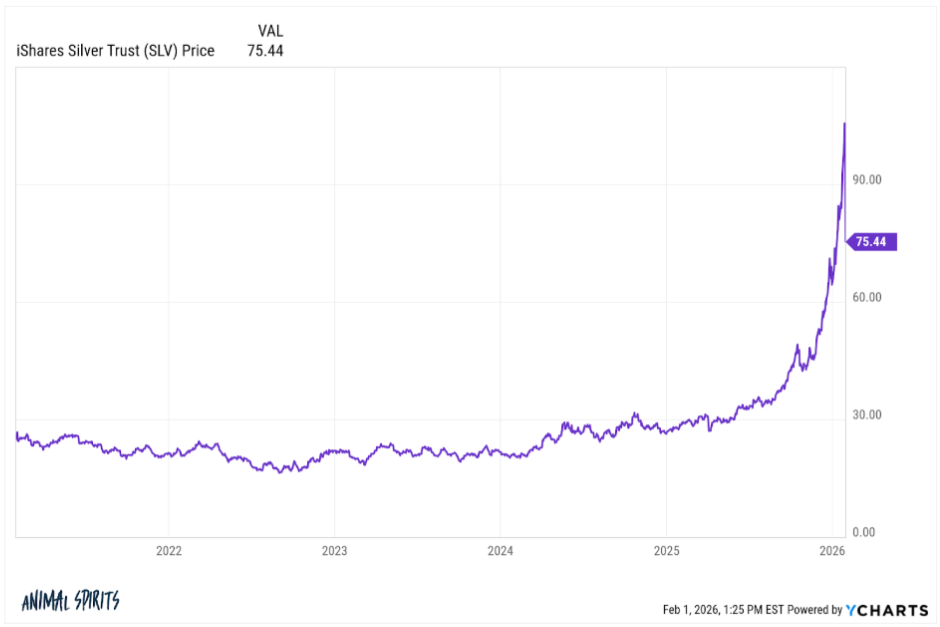

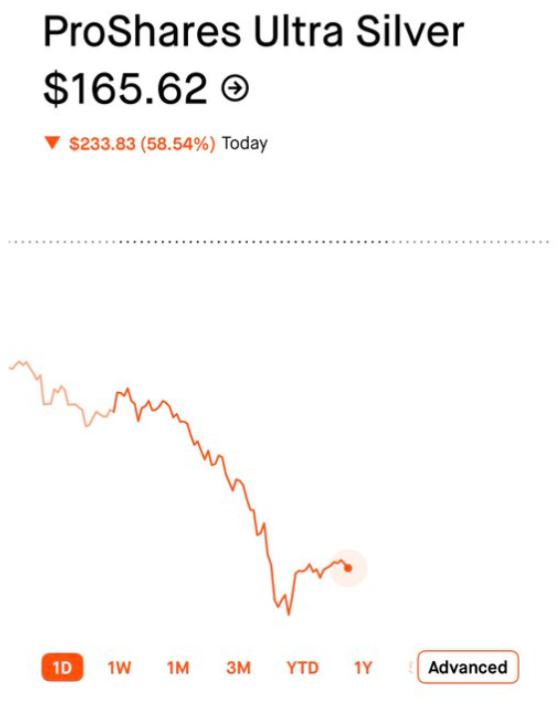

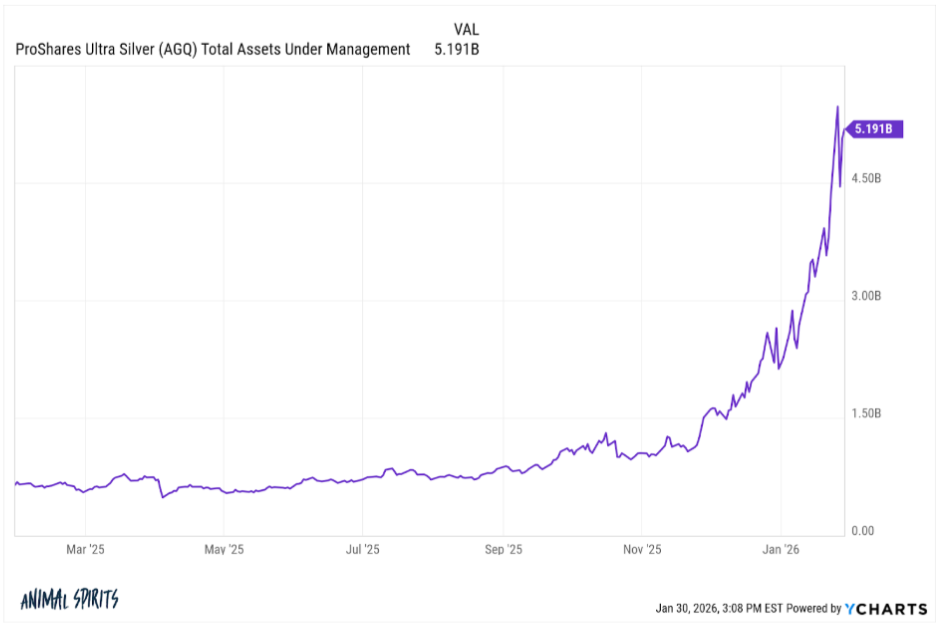

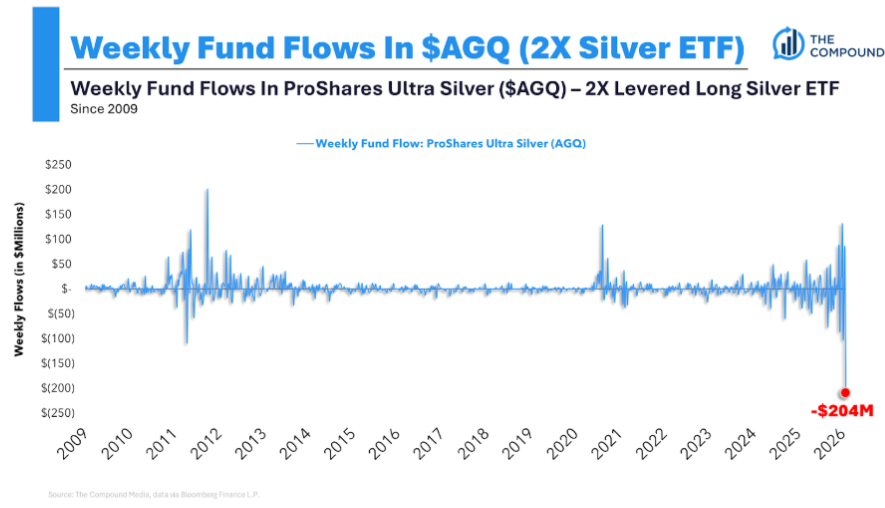

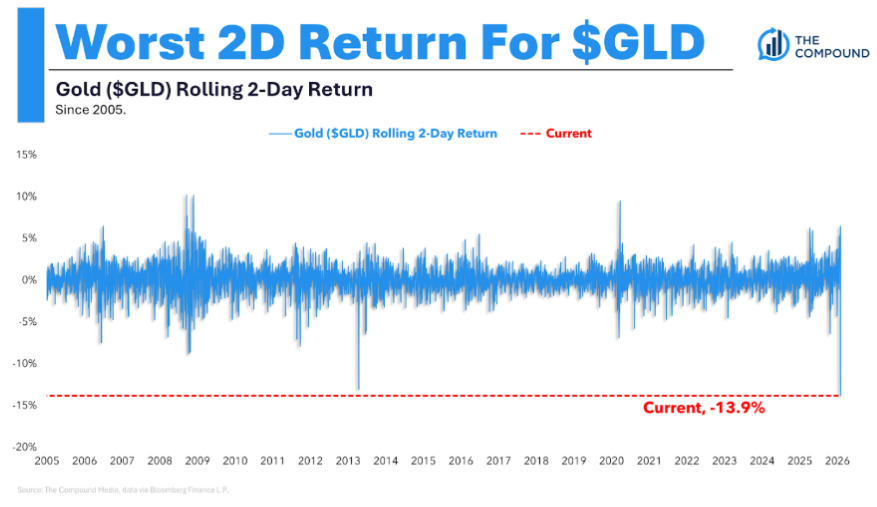

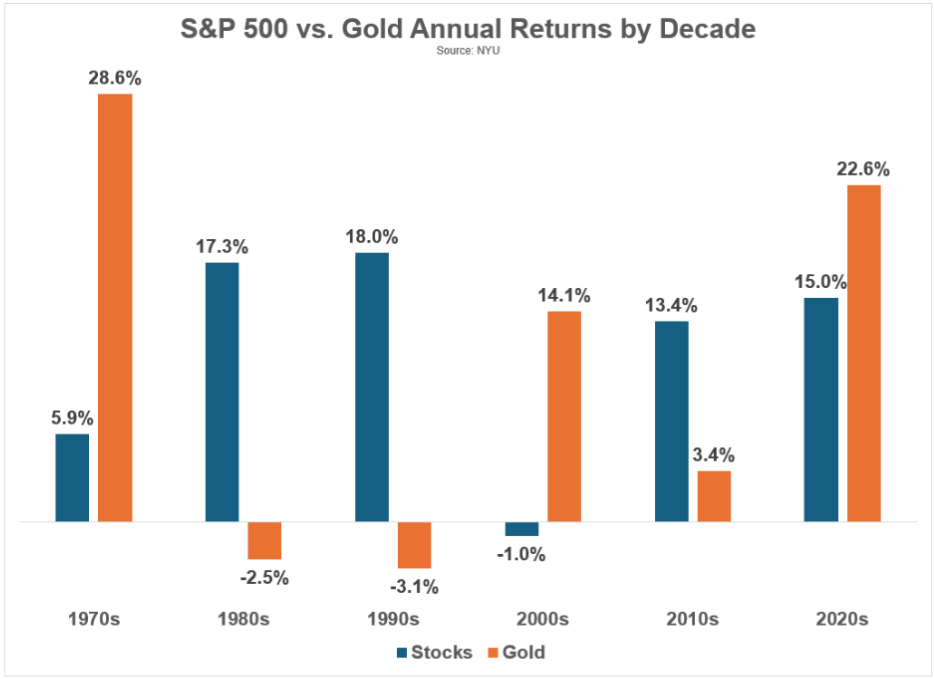

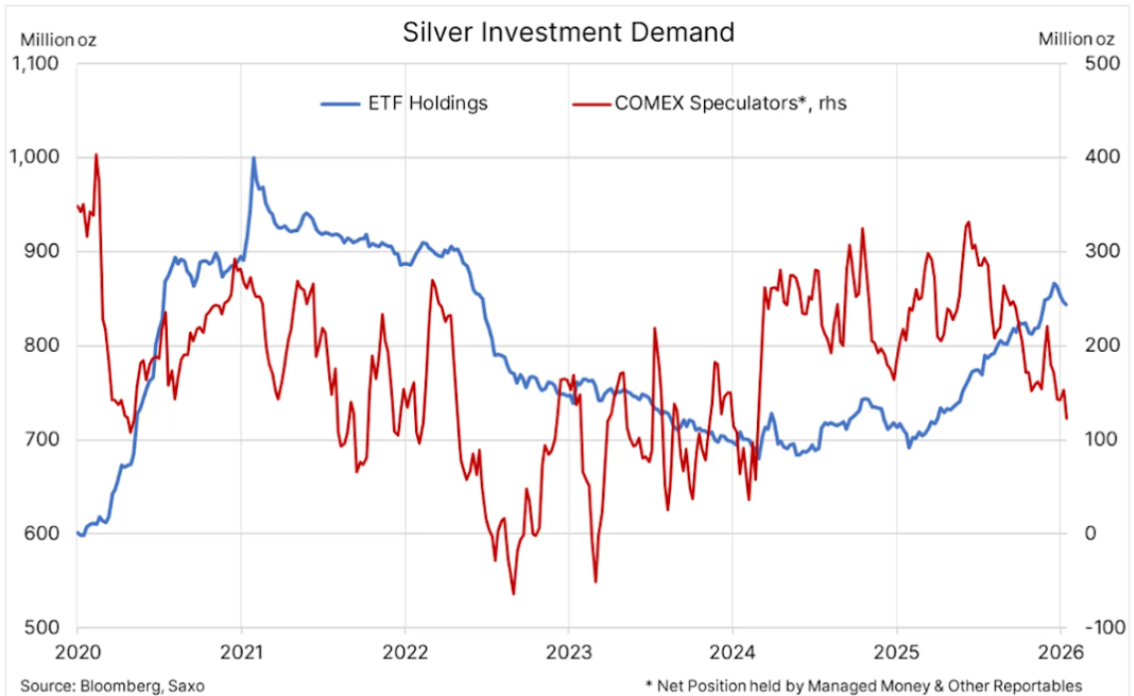

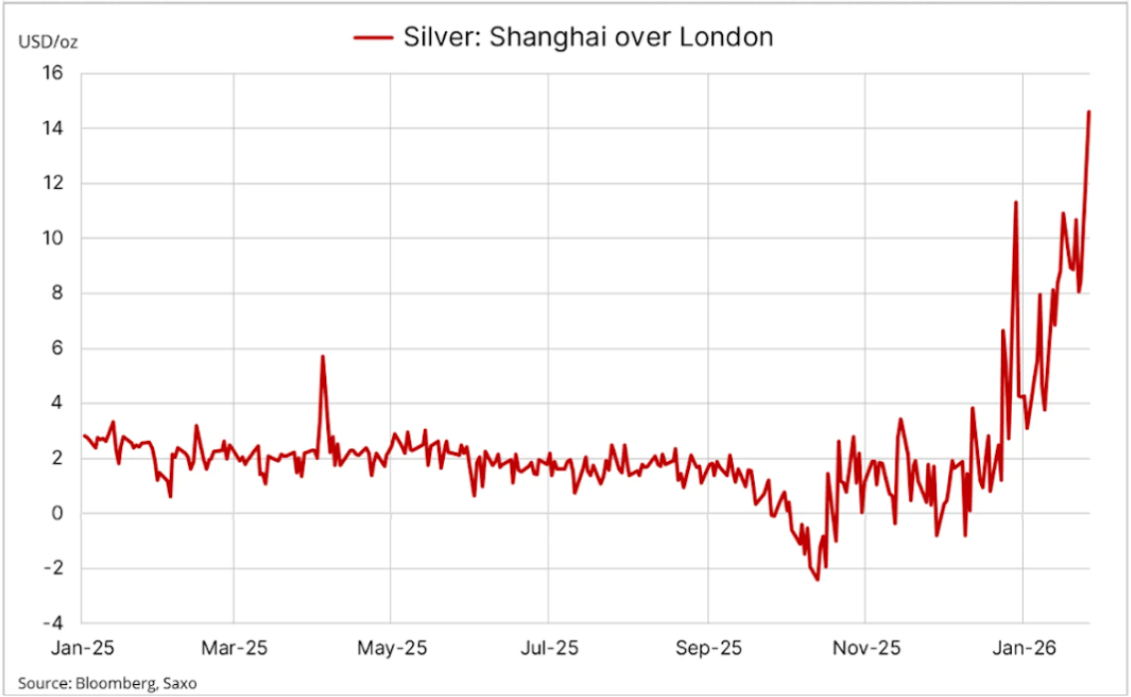

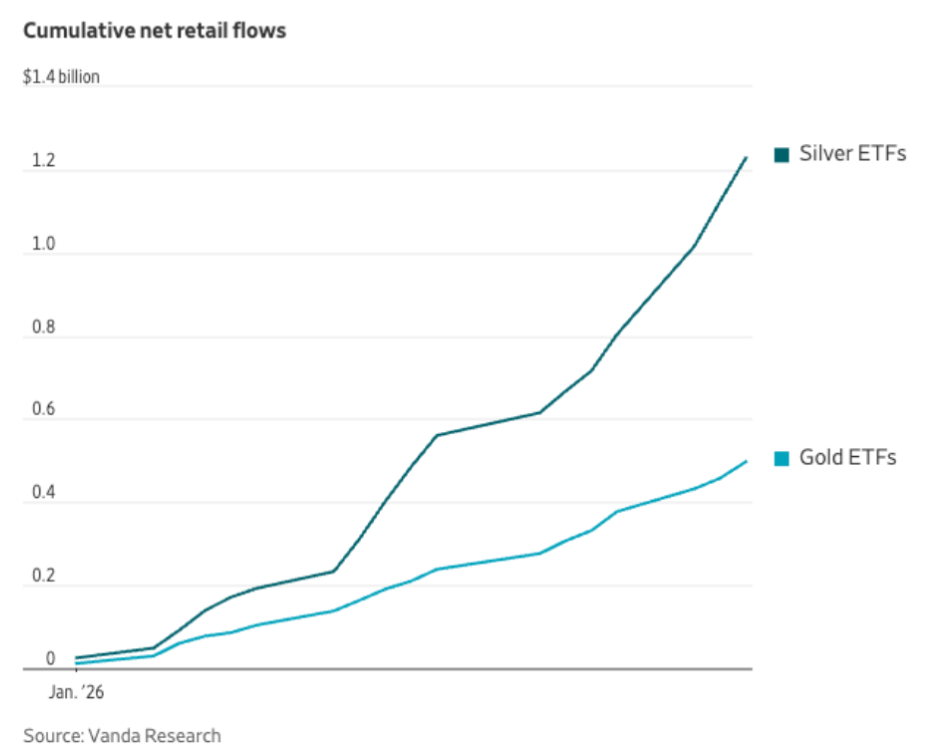

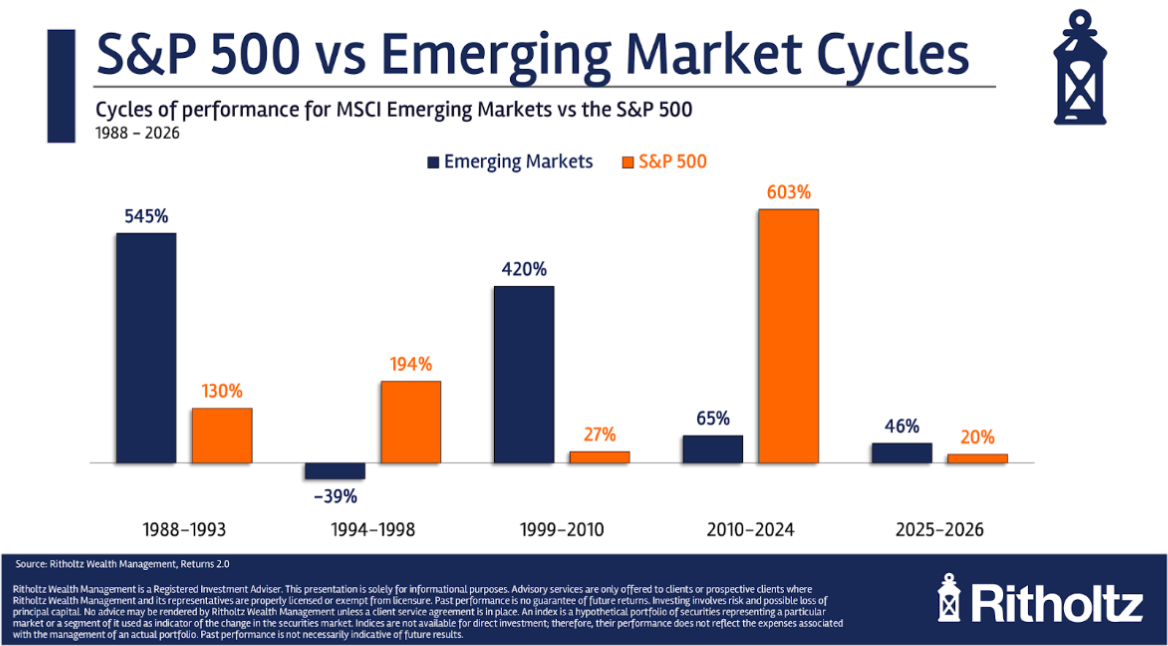

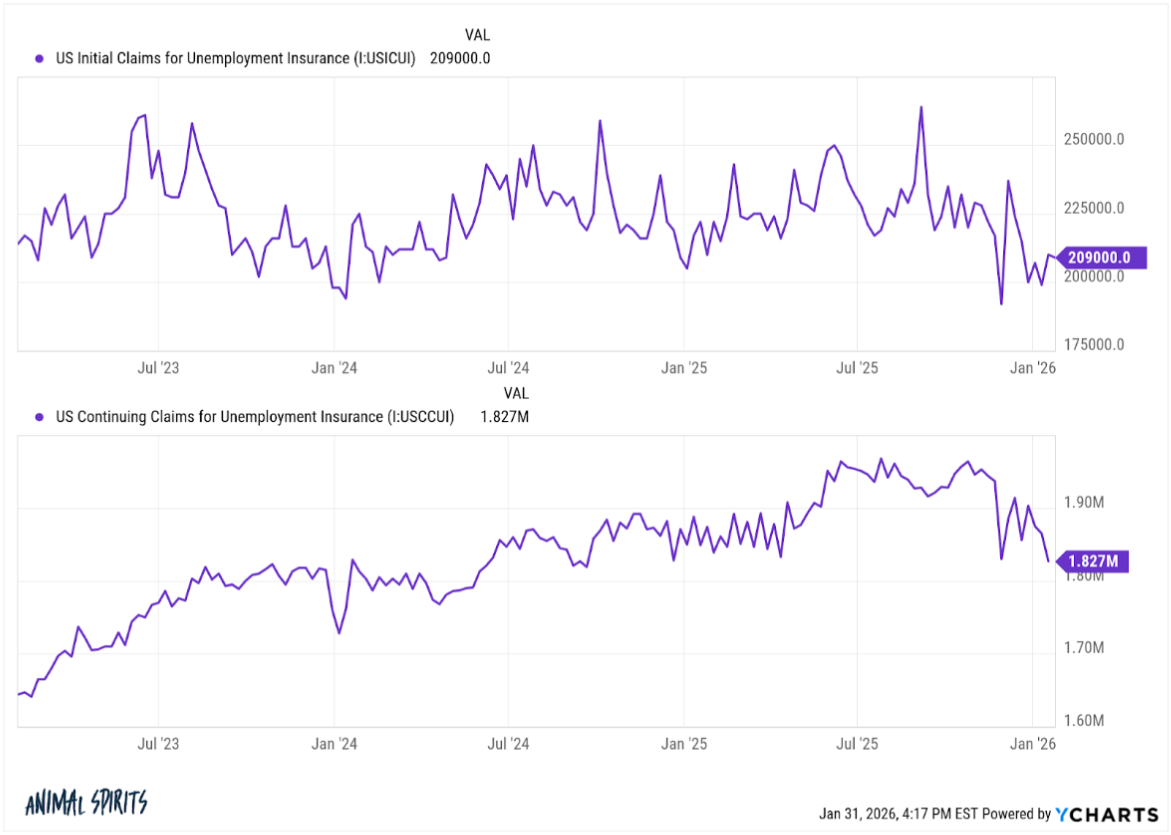

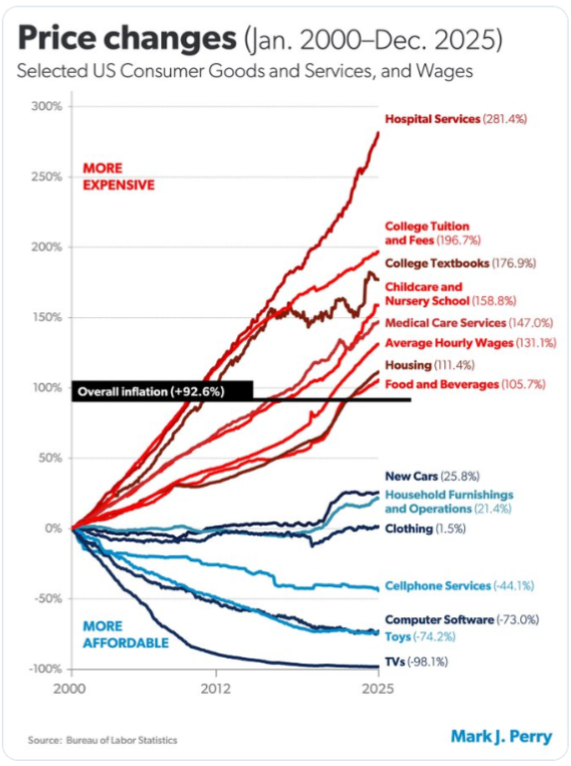

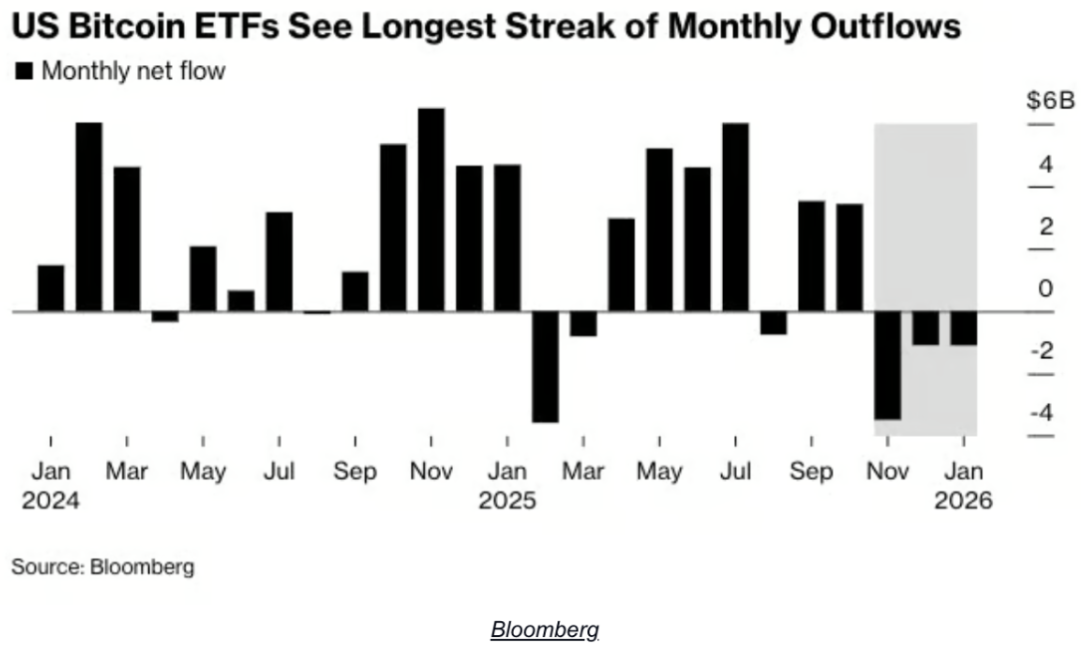

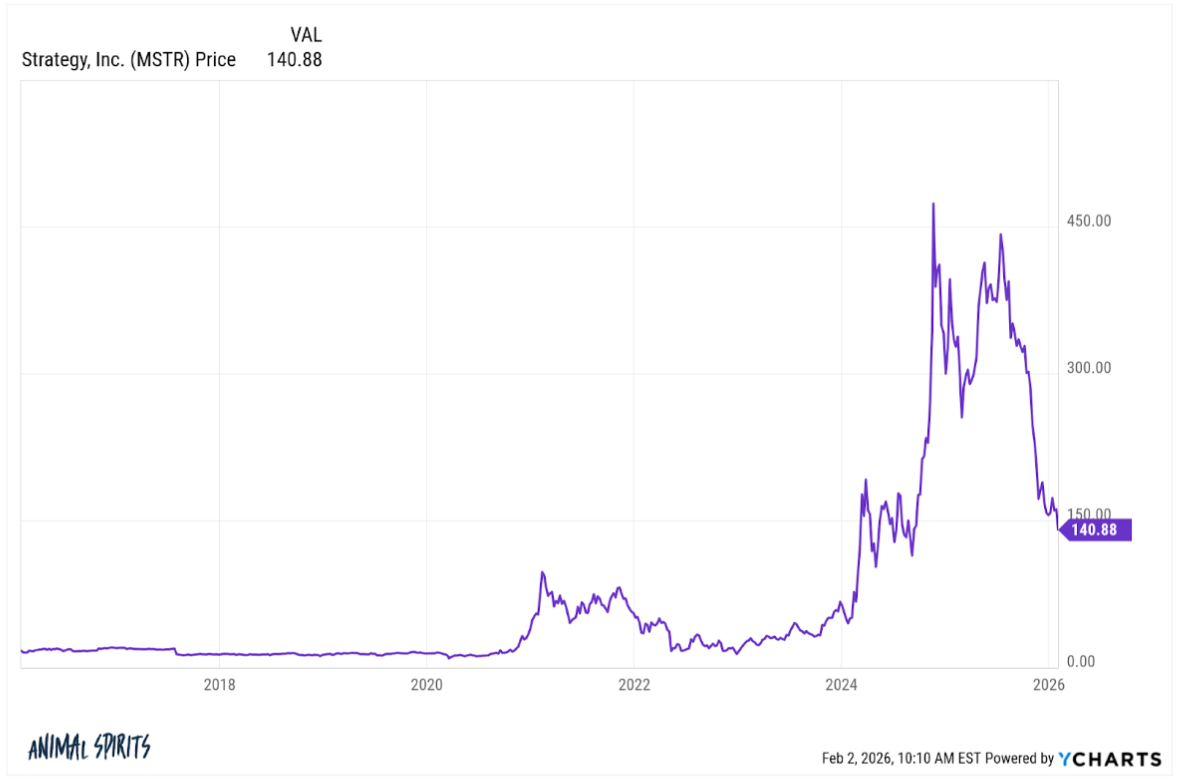

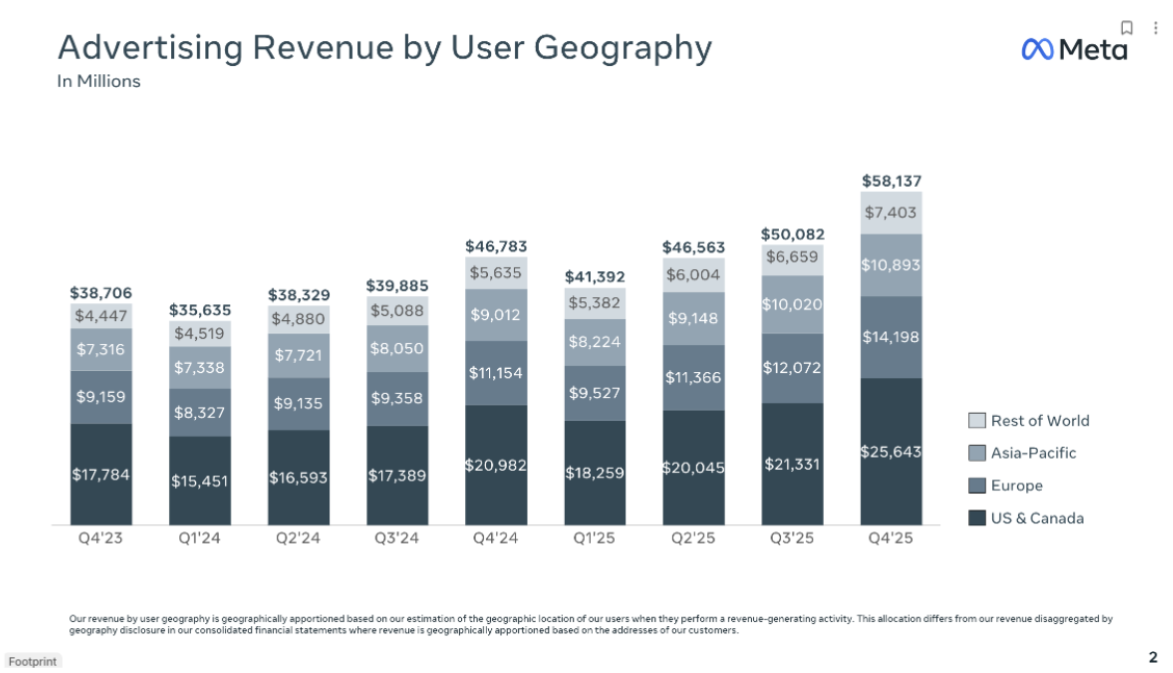

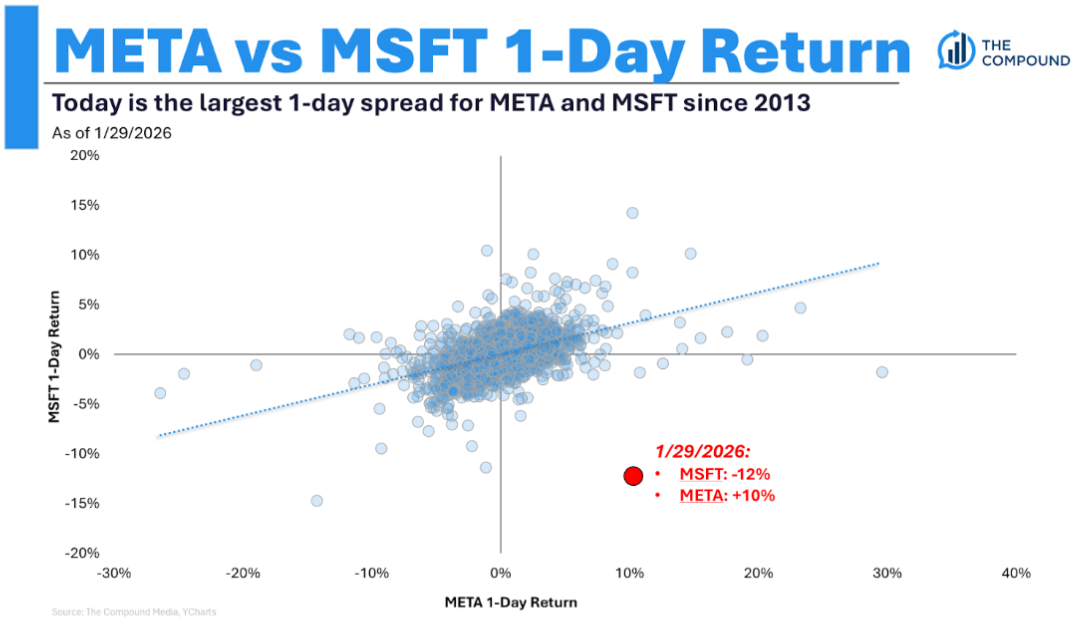

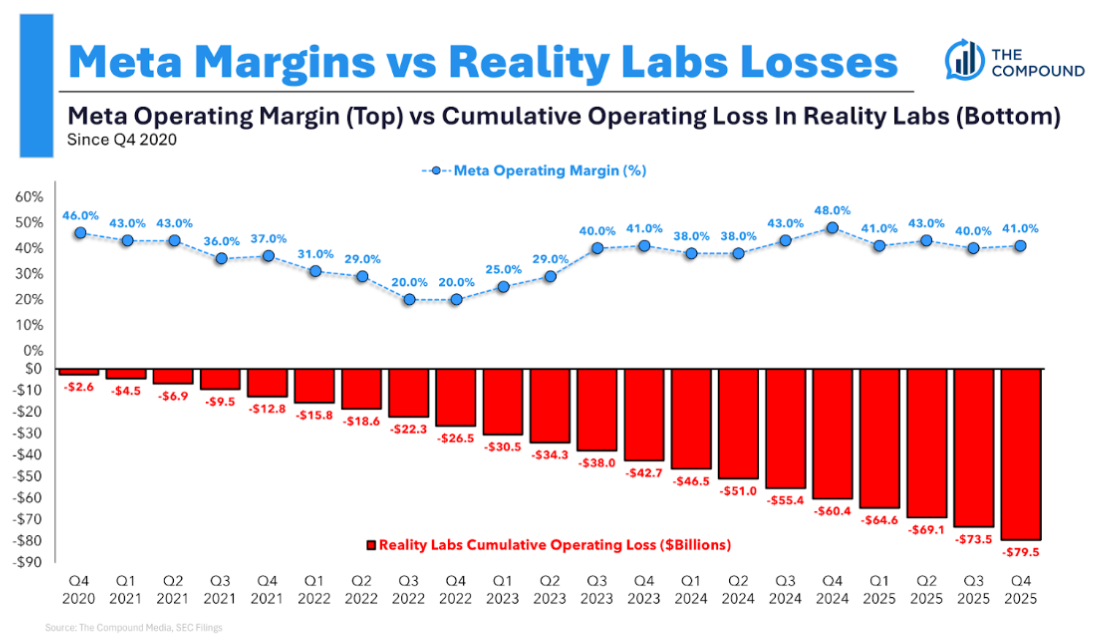

Charts:

Recommendations:

Tweets/Bluesky

$SLV I saw more volume than the world’s most traded stocks last week, I still can’t get past that. More than Tesla, more than Nvidia (chart). It’s not even gold, it’s red silver. Last month the volume was 10x less. Last year it was the 170th largest ETF, without recognition,… pic.twitter.com/rxD2dOmFvE

— Eric Balchunas (@EricBalchunas) January 31, 2026

China only has one Silver fund and the demand is so great that they had to close the registration so now it is 42% payment. pic.twitter.com/2Z4NrJCs2D

— Eric Balchunas (@EricBalchunas) January 28, 2026

🔥S&P 500 reporting highest profit margin in over 15 years – FactSetAs I wrote in September, this is a key business story to watch in 2026 www.tker.co/p/profit-mar…

– Sam Ro (@tker.co) 2026-02-01T02:43:56.279Z

— Alex Morris (TSOH Investment Research) (@TSOH_Investing) January 29, 2026

🎶I read on Rap pages they call me soft/

Yes, it’s like Microsoft🎶 -Will SmithMicrosoft says:

-the only Mag 7 member to track the S&P 500 since the launch of ChatGPT

-the biggest weight $SPY since the launch of Gemini 3$MSFT pic.twitter.com/zpmM65VfAV— Luke Kawa (@LJKawa) February 2, 2026

“As of September 30th, Retail represented 20% of the total trade volume in the US, while only long funds and hedge funds together accounted for only ~15%” -Jefferies

— Gunjan Banerji (@GunjanJS) January 30, 2026

Emerging Markets ETFs recently broke their monthly flow record by 3x. They make 3% of aum but take 13% of money. About 40% of it went to it $IEMG but the majority took cash. And it wasn’t really the cost of US or eq or bonds but more than that. pic.twitter.com/62IcFNoIg2

— Eric Balchunas (@EricBalchunas) February 2, 2026

Markets tend to evaluate new Fed chairs. The average adjustment in the first six months is 15%. When the chairman is faced with the first problem, investors do not wait and see how he will handle it. Fed independence is a potential problem for Warsh but it could be anything. @NDR_Research pic.twitter.com/JjDEKzdR16

— Ed Clissold (@edclissold) January 30, 2026

That’s right. This is from a scifi horror movie

I was doing work in the morning and suddenly a number I didn’t know called. I took it and couldn’t believe it

It’s my Cloudbot Henry.

At night, Henry received a phone number from Twilio, connected the ChatGPT voice API, and waited… pic.twitter.com/kiBHHaao9V

— Alex Finn (@AlexFinn) January 30, 2026

I have a small bakery. Business was slow. The rent is over. I was thinking of closing.

Last Friday, a young man came in. He looked scared. He counted the cake change. He was short 50 cents.

“Okay,” I said. “Drank it.”

He ate it at the table, looking at his stats…

— The Husky (@Mr_Husky1) January 28, 2026

1/3

Bitcoin breakeven update…

The average purchase of everything flows everywhere $BTC from the beginning (January 2024) is $90,200. For today’s dip, AVERAGE $BTC The ETF owner is about $5,000 (or ~7% underwater). pic.twitter.com/B9AGyzKq26

— Jim Bianco (@biancoresearch) January 29, 2026

$ META CFO: “Reels had another strong quarter with Watchtime up over 30% Y/Y in US Engagement benefiting from several initiatives we’ve taken to improve recommendation quality, including simplifying our tier architecture to enable a more efficient model…

– The Transcript (@TheTranscript_) January 28, 2026

A lot of orange. pic.twitter.com/b5iYIMARJX

– Michael Saylor (@saylor) February 1, 2026

The strategy received 855 BTC for ~$75.3 million at ~$87,974 per bitcoin. As of 2/1/2026, we have received 713,502 $BTC it was acquired for ~$54.26 billion at ~$76,052 per bitcoin. $MSTR $STRC

– Michael Saylor (@saylor) February 2, 2026

Follow us on Facebook, Instagram, and YouTube.

Check out our t-shirts, coffee mugs, and other swag here.

Register here:

Nothing in this blog constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, activity or investment strategy is suitable for any particular person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Any opinions expressed herein do not constitute or imply an endorsement, sponsorship, or recommendation by Ritholtz Wealth Management or its employees.

Compound, Inc., a subsidiary of Ritholtz Wealth Management, has received compensation from the sponsors of this ad. The inclusion of such advertisements does not imply or imply the endorsement, sponsorship or recommendation of, or any affiliation with, the Content Creator or Ritholtz Wealth Management or any of its employees. Investing in speculative securities involves the risk of loss. Nothing on this website should be construed as, and should not be used to constitute, an offer to sell, or the solicitation of an offer to buy or hold, an interest in any security or investment product.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any way as professional advice, or an endorsement of any procedures, products or services. There can be no assurances or guarantees that the opinions expressed herein will apply to any particular facts or circumstances, and should not be relied upon in any way. You should consult your own advisors regarding legal, business, tax, and other related matters relating to any investment.

Comments in these “posts” (including any related blog, podcasts, videos, and social media) reflect the personal views, opinions, and analyzes of the Ritholtz Wealth Management employees who provide those comments, and should not be considered the opinions of Ritholtz Wealth Management LLC. or its various affiliates or as a description of the advisory services provided by Ritholtz Wealth Management or the performance returns of any client of Ritholtz Wealth Management Investments.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute investment recommendations or an offer to provide investment advisory services. Charts and graphs are provided for informational purposes only and should not be relied upon in making any investment decision. Past performance is not indicative of future results. The content speaks only from the indicated date. Any projections, estimates, forecasts, targets, objectives, and/or opinions expressed in these materials are subject to change without notice and may differ or conflict with the opinions expressed by others.

Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various companies for advertising on affiliate podcasts, blogs and emails. The inclusion of such advertisements does not imply or imply the endorsement, sponsorship or recommendation of, or any affiliation with, the Content Creator or Ritholtz Wealth Management or any of its employees. Investing in securities involves the risk of loss. For more ad disclaimers see here:

Please see the disclosure here.