How Much Will Your Long Term Needs Cost? It Depends on How Much You Rate – Center for Retirement Research

The consulting company Milliman recently published the Long-Term Care Index 2025, calculating that – on average – people aged 65 years should set aside $ 135,000 for their long-term care needs.

Great Diversity

While the average figure can be a useful reference point, Milliman’s estimates show considerable variation based on gender, location, and health status, among other factors. For example, the average cost for women is $171,000 and for men is $98,000, mainly because women live longer. As a result, they may require long-term care and are less likely to have a spouse available to help them without cost.

According to Milliman, about half of men and four out of ten women will not need paid care at all during their lifetime. Another quarter of men will receive less than a year of paid care, leaving only 29 percent who need more than a year of paid care. Women, on the other hand, are more likely to need long-term care with 41 percent facing more than a year and 14 percent needing five years or more, which will cost them a whopping $665,000 (see Figure 1).

I should note that the Milliman calculations assume that all maintenance paid to take care of. The Center for Retirement Research at Boston College estimated that families typically provide at least half the hours of caregiving, even for those with the highest needs. Milliman also does not say how these costs are paid, specifically whether they include Medicaid-covered care or out-of-pocket costs.

Location, Location, Location

Costs vary greatly by the type of care needed — home health, assisted living, or nursing home — and location. Location is not only important in terms of maintenance costs but also longevity and health. People live longer (and, therefore, may need care longer) in some states – such as Hawaii, California, Washington, Florida and New Hampshire – than in others – such as Mississippi, Alabama, West Virginia, Louisiana and Kentucky.

On the other hand, people in good health tend to need less care. Milliman highlights Colorado, Montana and Hawaii as states where residents are least likely to need any paid health care and Montana, too, and Arizona and Oklahoma as states where people need the least amount of care. At the other end of the spectrum, those with care needs in Hawaii, Connecticut and New York receive care for the longest time.

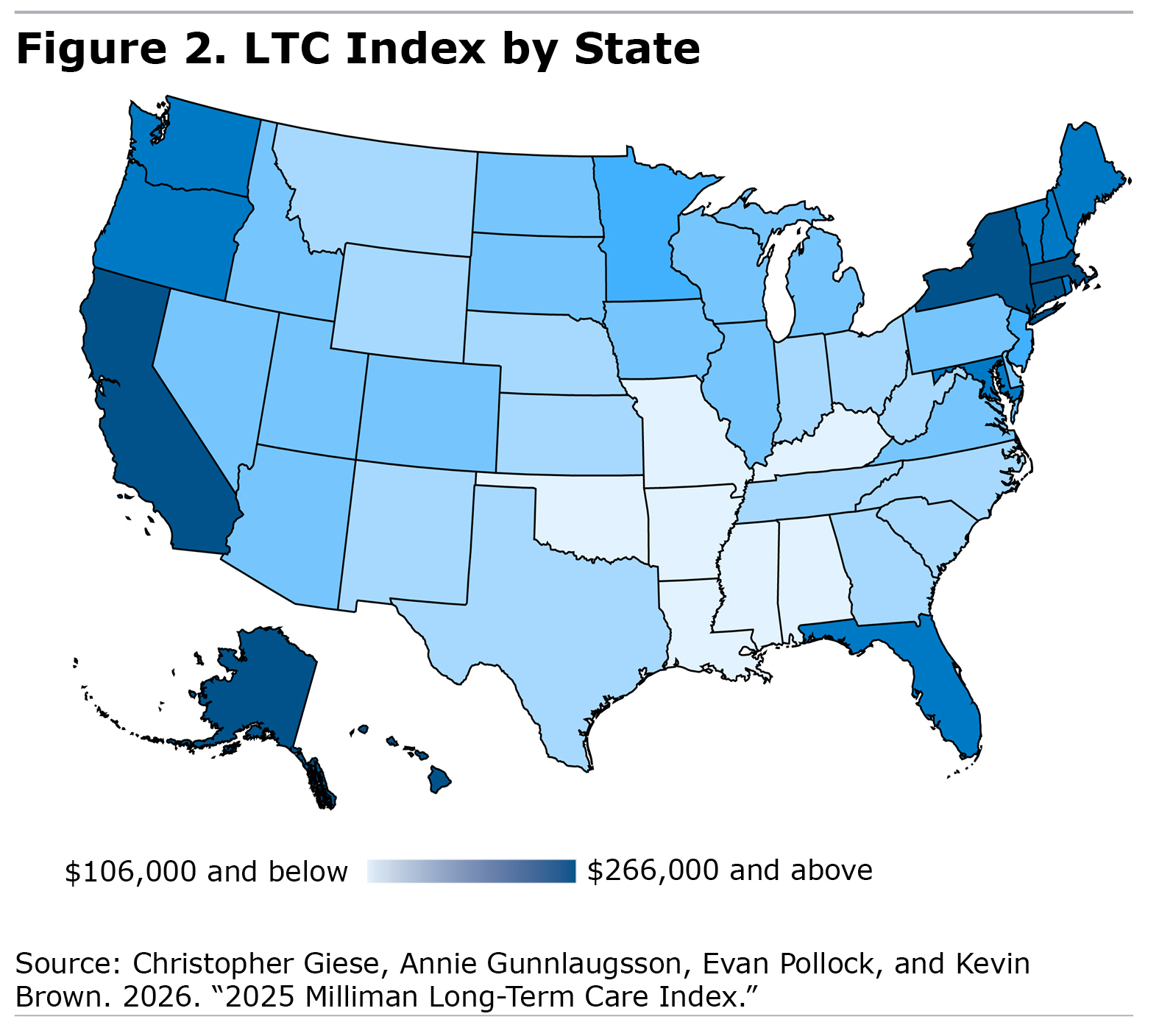

Combining all these factors – so that the cost of LTC services, the likelihood of needing services, and the duration of needs are calculated – Figure 2 shows Milliman’s ranking of the average cost of long-term care in each state (see Figure 2).

The most expensive regions (in blue) are on the West Coast and Northeast, where average costs are nearly double the national average. The lowest costs are found in the South-Central region (blue).

Another factor that determines how much a 65-year-old should set aside for care is the expected rate of return. The $135,000 estimate is based on an average investment return of 4.35 percent. Using the higher rate of 7 percent, a 65-year-old person will only need to put aside $74,000, but using the lower rate of return of three percent, he will need $187,000 in the bank.

What Does This Mean To You?

For individuals and families planning for long-term care expenses, it can be difficult to anticipate the need. I’ve written before about the factors that affect the need for paid long-term care, including lifespan, family history, and family situation.

But the $135,000 figure seems like a good starting point. Increase that number if you live in an expensive area, have a family history of dementia or other illnesses that may require long-term help, or if you don’t have family members who can help.

Your current health may have a positive or negative effect on the number. If you already have a chronic debilitating disease that you can live with for many years, such as Parkinson’s, you can expect to need more money. But if you have a type of cancer that can shorten your life but not lead to a long period of disability, you may need much less.

Insurance Solution?

My main takeaway from the Milliman report is that we need a universal long-term care insurance plan since we have so much uncertainty about individual needs combined with relative uncertainty about those of all seniors. Furthermore, while a minority of the elderly can afford the cost of their care, whatever it may be, the majority cannot.

According to the Federal Reserve, the average retirement savings for 65- to 74-year-olds in the United States is $200,000, which means half are below this amount. People age 75+ have an average savings of just $130,000. In short, many baby boomers likely don’t have enough money to cover their long-term care costs.

The cost of taking care of long-term needs can be much lower if we start contributing at an early age through the national insurance system. With its 4.35 percent rate of return, Milliman calculates that a 35-year-old would need to set aside $38,000, on average, to cover their long-term care costs, about $100,000 less than a 65-year-old. Of course, few 35-year-olds think about their future care needs, but together we can face this challenge. In fact, Washington State has set up such a program, which provides a basis for long-term care protection for its employees (up to $36,500); and is exploring ways to allow people to purchase additional long-term care insurance at a group rate. Several other states, including Massachusetts, are already testing similar programs.

For more from Harry Margolis, check out his Risking Old Age in America blog and podcast. He also answers consumer property planning questions on AskHarry.info. To stay updated on the Squared Away blog, join our free mailing list.