Understand Passive Investing Data

I prefer to invest my time diligently and my money passively. But many investors think they can add value to their investments when they can’t. This is a big problem. In fact, spending a lot of time and effort on their investment, on the contrary, can take away the value (not even the value of their time) while adding an additional tax burden of effective strategies.

However, once people realize the benefits of passive investing, they sometimes “jump the shark” about it. You can take this concept too far.

Passive Investing Data

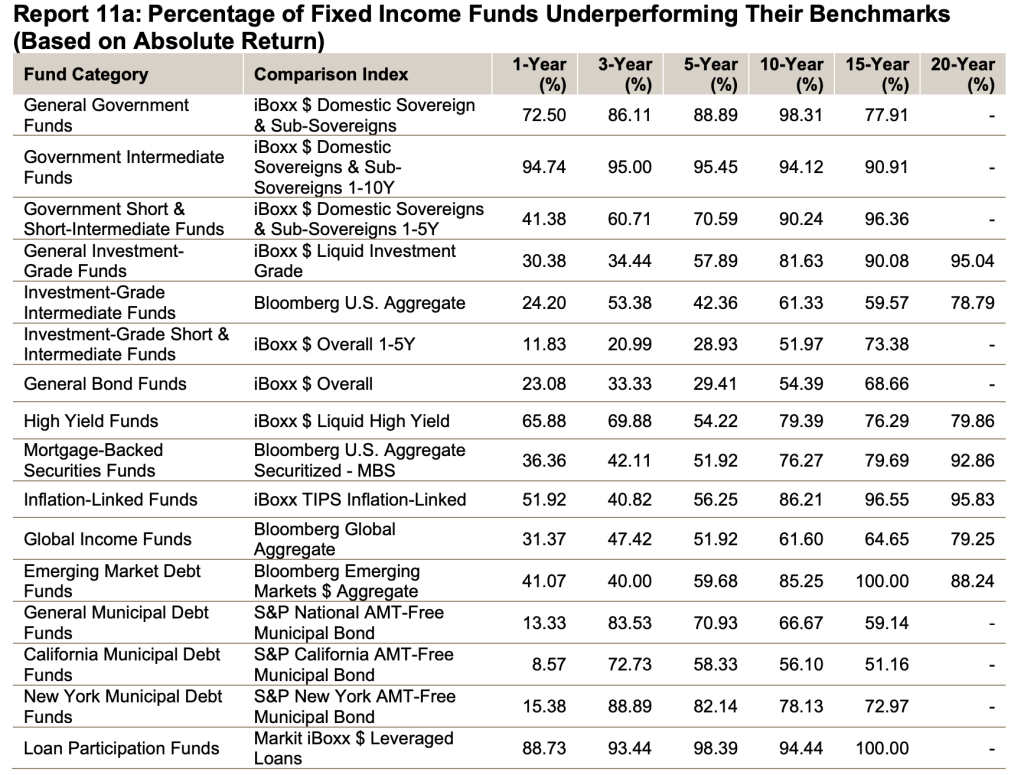

Perhaps the greatest demonstration of the benefits of passive investing comes from the annual SPIVA reports. Here’s a chart from the most recent when I wrote this post, but trust me when I say they’ve all looked pretty much the same for years and years.

Basically, over the long term, most actively managed stock funds underperform their index. Since an index fund is just like an index, index funds will outperform the vast majority (90%+) of mutual funds in long-term performance before taxes. After taxes, the data looks even worse for executives. That’s all. That’s all you can say about being active and not doing anything. The best way to invest in stocks for most investors is to use index funds. It beats the pants on picking active managers, let alone being your own active manager by picking your own stocks.

However, it is important to understand WHY this is so. Here are a few reasons why I rate them higher or lower in order:

- Low cost

- A few moral lapses

- Low profit

- Minimum term requirements and potential advisory fees

- Wide variety

- Low taxes

Mainly, it is low cost. You don’t need to pay for all the buying and selling and analysis and labor. Investment advisors who use index funds tend to charge less, too. The result of a lower tax bill due to the avoidance of capital gains distributions, especially short-term gains, is because of those lower profits. These factors are all still important as you move from investing. In fact, they are more important than whether the investment is working or not. Let me give you a couple of examples where people get too carried away about useless investing.

More info here:

Do People Still Believe in Effective Management?

10 Reasons to Invest in Index Funds

Vanguard Bond Funds

I received an email recently that read:

“I’ve been your student for over 10 years. If I may be nosy, for muni bond funds I believe you prefer VWIUX over VTEAX? I’m curious why VWIUX is listed as Vanguard, while VTEAX is listed as passive…

VWIUX is a Vanguard Intermediate-Exempt Bond Fund. It has an expense ratio of 0.17%, holds more than 15,000 bonds with an average maturity of nearly six years, and has a yield of 20%. It is an actively managed bond fund, like many of Vanguard’s best bond funds.

VTEAX is a Vanguard-Exempt Bond fund. It has an expense ratio of 0.07%, has approximately 10,000 bonds with an average maturity of 7.2 years, and has a yield of 22.8%. It is technically a passively managed bond fund. It is an indicator bag.

I have no choice between these funds and I treat them as the same. They are our tax loss harvesting partners in my portfolio, and at the time I got the email, our muni bond funds were actually in VTEAX. But when I started buying medium-term municipal bonds, VTEAX didn’t exist. So, we used VWIUX. To be honest, the most important difference between the two is a small difference in time, not a difference in cost or management style. Meanwhile, five-year yields were 0.74% versus 0.07%, and the big difference was explained by VWIUX’s short duration, which collides with a quick, big hike in interest rates back in 2022.

It’s important to understand WHY doing nothing is often better than working, so you can see when it doesn’t matter that much (and any exceptions). Note also that the data on transaction performance is not as strong among bond funds as among stock funds.

Hypersensitivity to Costs

Another thing I often see among passive investor investors is being overly sensitive to costs. They think that a difference of a few basis points is significant. They don’t, as I wrote here back in 2018 when Fidelity came out with their Zero index funds with a 0% expense ratio. Back then, everyone was wondering if they should switch their Vanguard index funds with 0.03% or 0.05% expense ratios to Fidelity with 0% expense ratios. A quick look at the performance tape from that time shows that I was right to tell people not to worry too much about it. I have used both funds over the years with very similar performance. The five-year performance numbers for high-quality index funds are consistent.

- FZROX (Fidelity Zero Total Stock Market): 12.94%

- FSKAX (Fidelity Total Stock Market Index Fund which charges a minimum expense ratio): 12.67%

- VTSEX (Vanguard Total Stock Market): 12.66%

- ITOT (iShares Total Stock Market ETF):13.07%

That’s a rounding error with respect to performance. Most will conclude that the operating profit is not worth the fund having to be held at Fidelity and the additional tax costs due to not having an ETF share class to extract capital gains. Of course, you shouldn’t be aware of any unnecessary big gains to change currencies. A similar story is seen on the international stock side:

- FZILX (Fidelity Zero Total International Stock Market): 10.22%

- FTIHX (Fidelity Total International Stock Market Index Fund with minimum expense ratio): 9.69%

- VTIAX (Vanguard Total International Stock Market): 9.80%

- IXUS (Shares Total International Stock Market ETF): 7.92%

Don’t focus too much on the cost. Once you get below about 10 points, you are investing for free. The difference in the tracking index is probably more important than the average cost. If everything were a cost ratio, the difference between the various currencies would reflect a difference in the cost ratio, and that is not the case. Zero fees can be done gradually over the next five years (and there was a period in 2019 and 2020 when they did).

DFA and Avantis Funds/ETF

I also laugh when I see people mock funds/ETFs like those from DFA and Avantis as bad because they are “actively managed.” Well, kind of. The argument made by these fund companies is that they use an active implementation of the passive philosophy.

They see where real index funds do little things that cost their investors money and try to avoid doing those things. Does it work? The jury is still out, but it’s not hard to compare performance numbers. The closest thing Avantis has to a comprehensive stock market ETF (AVUS) compares favorably to Vanguard’s VTI.

AVUS has 1,940 US stocks, a dividend yield of 1%, a P/E ratio of 22.93, an expense ratio of 0.15%, and a five-year return of 14.39%.

VTI has 3,511 US stocks, a dividend yield of 2.1%, a P/E ratio of 27.3, an expense ratio of 0.03%, and a five-year return of 12.66%.

I would argue that the main difference is that the average stock in AVUS is smaller and more valuable than the average stock in VTI. I would NOT argue that AVUS is a poorly managed fund. That is just an assertion.

Markets Without Index Funds

It gets even worse when you get into markets/asset classes where index funds don’t exist at all. Imagine you want to invest in cryptoassets or precious metals. There is no index bag. There is no private equity or private equity index fund, either. If you want to invest in these asset classes, you basically go back five decades to a time before index funds existed. You may be very happy to get a “market return” for an asset class, but there is no way to guarantee that. You must hire an active manager or be the manager yourself.

Yet I see people trying to compare private real estate returns to index fund returns and deride real estate investors as the equivalent of stock pickers. There is no alternative in the inheritance category. You can avoid the asset class for that reason, or you can, like me, do the equivalent of buying an index fund. You choose experienced managers, diversify widely, keep costs (including taxes) low, manage your investments, and move forward. You may also note that active management may still apply to these asset classes, at least to a greater extent than in the publicly traded stock world.

The reason active stock fund managers can’t beat index funds more often isn’t because they stink. It is because they are so beautiful and so many. Therefore, passive investors get a free ride in a highly efficient market. This is not necessarily the case in less analyzed markets such as your local market.

If you see a $100 bill on the floor, pick it up. There are more of them when there are 10 investors competing against a bunch of average Joe homeowners than when there are 100 million investors competing against each other.

More info here:

The White Coat Investor Buys Individual Stocks — The M&M Conference

Choosing Individual Goods is a Losing Game

Nonsense

Sometimes, I even see people trying to apply the “active is bad” mantra to things that have nothing to do with investing. Like estate planning or running your business or taking steps to reduce taxes. Ignoring your rental properties when you can’t expand the living space or increase their value is foolish. Add value where you can.

The Bottom Line

Passive investing works, especially in the publicly traded stock market. But be careful not to stretch the idea too far. It’s also important to understand WHY index funds perform better than actively managed funds and apply those principles to all of your investing activities.

WHAT DO YOU THINK? When are you convinced of the worth of passive investing? Have you ever found yourself “jumping the shark” in the sense of “be a passive person, do nothing?”