Marriage Can Be Good for Your Finances – but Avoid These Three Mistakes – Center for Retirement Research

What could go wrong? Being a couple makes it difficult to make your own decisions.

According to an economist, another benefit of marriage is financial benefits. Marriage allows risk sharing between partners (eg, one partner can work more if the other loses a job) and allows couples to take advantage of economies of scale (ie, it is cheaper to maintain one household than two separate ones). These benefits are why I find the nearly 30 percent decline in marriage rates over the past 40 years troubling.

But marriage also makes it difficult to make financial decisions. Singles may delay big decisions like saving for retirement. Once married, couples should realize that retirement savings should be shared between two people, not just one. Also, decisions about this saving should reflect two sets of personalities and preferences.

The truth is that couples – and this may include you – often make mistakes. Research I conducted with my colleagues Alicia Munnell and Wenliang Hou found that although married couples were financially beneficial to the marriage. high risk having insufficient retirement income to maintain their standard of living before retirement. So, what’s wrong? A few things that people can resolve to fix themselves in the new year, start before the couple gets married.

Error 1: Waiting Until Marriage…last

Along with falling marriage rates, people are getting married later. Since marriage is a milestone that often separates youth from adulthood, the logical question is how this delay affects retirement savings. Such delays may deprive individuals of years of contributions, employer matching, and compound interest.

To test this issue, a study I conducted back in 2019 linked marriage data to 401(k) savings and followed people before and after their marriages. The study found that men are 13 percent more likely to participate in a 401(k) after marriage and that, when they do participate, they contribute 6 percent more. For women, the benefits of participating in marriage were smaller – 5 percent – but their contribution is more beneficial, at 17 percent. Therefore, if the trend of delayed marriage continues, it could lead to saving delays as well.

Plan: Start saving now…no matter what your relationship status is.

Mistake 2: Forgetting You Can Keep Two

Once married, couples would do well to remember the obvious: you are now two people tied together financially. Therefore, a two-income couple needs to save more for retirement than a one-income couple, since they need to change their total income. But here’s the thing: while retirement needs are a household problem, saving for retirement tends to be individual. Most people make savings decisions while at work and without their spouses. Or, they may follow their program’s defaults. These options may be appropriate if both earners have retirement plans at work. But, if one member of the couple earns money but doesn’t have a 401(k), their spouse needs to save more to replace that money. However, the research I worked on with Wenliang Hou showed that they do not. Families with two earners but one 401(k) save about half of other couples relative to their income (see Figure 1). In other words, the saver fails to recognize that it is saving two.

A two-reward couples program: Make sure you know when the other member is saving and, if not, save more.

Mistake 3: Taking on the Personality of a Spouse Who Is Too Insecure

Everyone who is currently married knows the key left marriage is easy: compromise. But, the research I found shows the negative – sometimes people with good financial habits accept their partners who don’t have good financial habits.

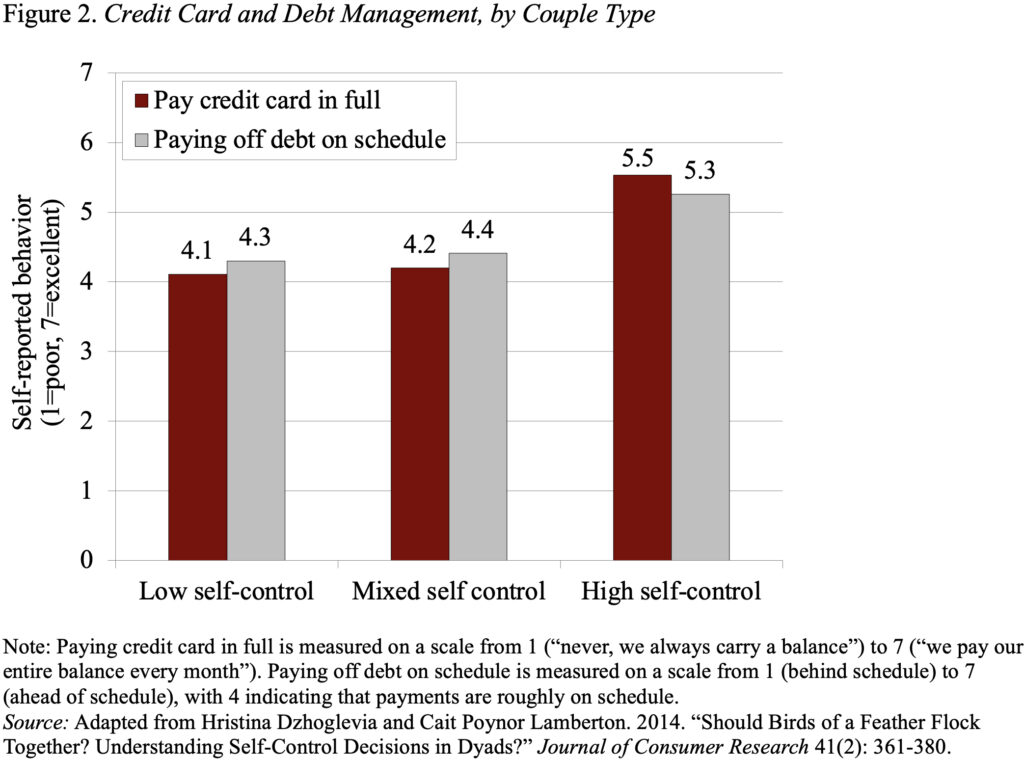

To measure ability, the study assessed the couple’s ability to control themselves. After all, research consistently shows that people with less self-discipline save less, have more debt, and make poor financial decisions. The couple was then identified as having two members with high self-control, two members with low self-control, or being a mixed-control couple.

Figure 2 shows one of the key results. When people were asked to report on a scale from 1 (poor) to 7 (excellent) how often they paid their credit cards in full or their bills on time, couples with high self-control fared better than couples with low self-control. It’s not surprising. But, surprisingly, the mixed abstinence couples looked just like the low abstinence couples. It seems that when they try to be a good spouse and accept their controlling spouse, the more controlling spouse allows their finances to suffer.

A plan for high self-control spouses with low self-control spouses: Try working with your spouse to ensure that some of your good financial habits shine through.

And a lesson for everyone: make sure you avoid these three common mistakes.