5 ways to simplify and reinvent your insurance business | Insurance Blog

In the face of continued disruption, insurers are called upon to reinvent themselves. To evolve at the operational level, insurers need to move from complexity to simplicity. This in itself is a difficult task. Integral architecture helps insurers to simplify these complexities at every step of the insurance value chain, often using processes they already have in place. Below are 5 practical use cases for compound structures.

1. Policy management – from complex organizational structures to outdated and integrated ecosystems

Many services for new insurance applications can be discovered. This will enable insurers to apply through digital portals and an AI-based product/coverage selection engine. This can also help them establish a pre-qualification engine based on data from various vendors such as distance to shore, CLUE reporting, risk assessment using IOT sensors (Surveillance Systems, Smart Home Devices, Smart Metering, etc.), and external pricing and rating engines. This helps in disseminating development, integration, and testing efforts and applying new business policy at a faster pace. Splitting processes into multiple sub-processes helps users to use them at different points in the policy transaction timeline such as when creating a financial verification, or during a renewal.

View the big picture

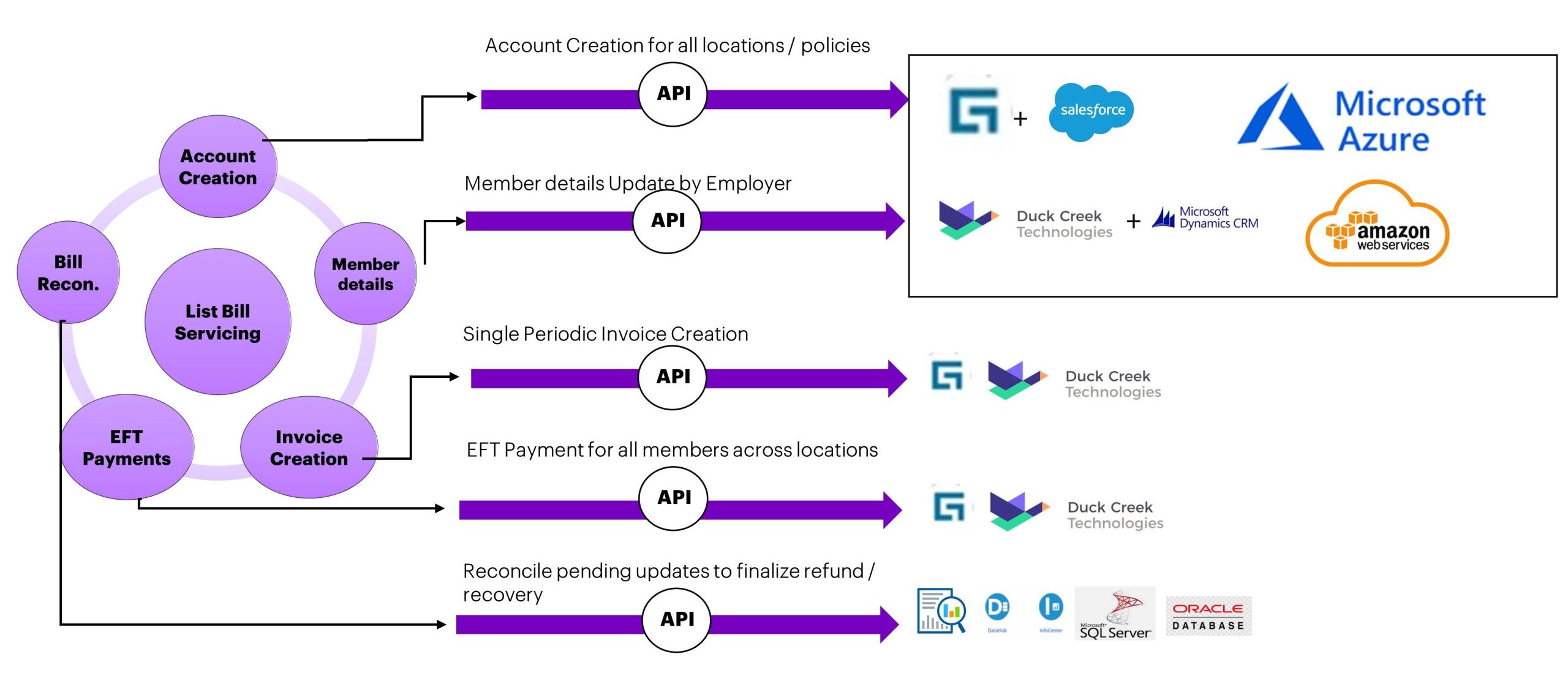

2. Payment management – from manual to automatic and personalized invoices

In the case of payment management, the bill list service classification can be used to create reusable tasks such as account creation and member information updates. Invoice is generated for transactions to all multiple policy holders or agents, periodically and EFT payments are completed to different policy members across locations. Refunds and refunds can be made based on research activities completed at the end of the policy year. Many of these individual services are also used in general testing of commercial lines as well.

View the big picture

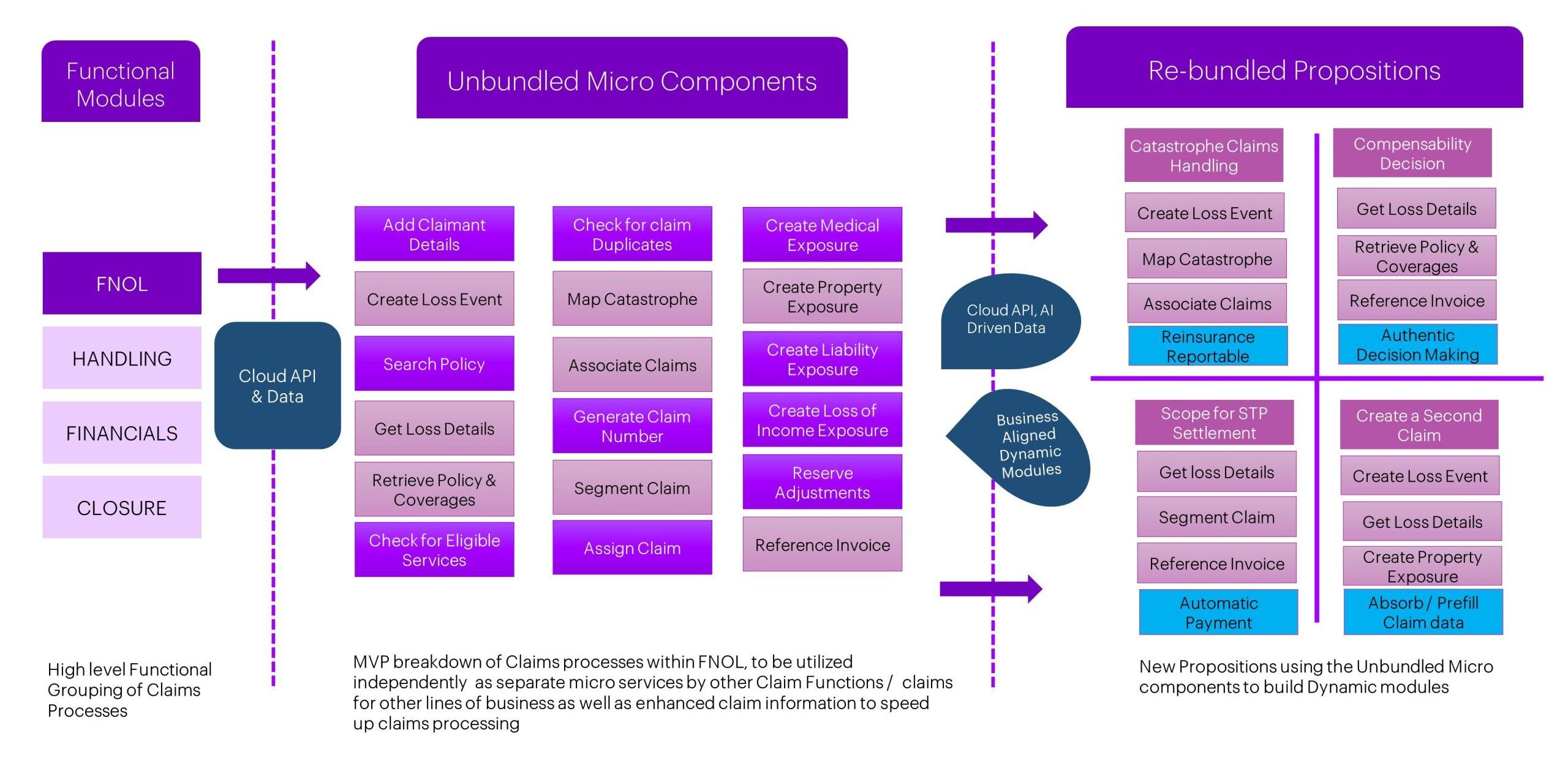

3. Transforming claims in harmony – from flexibility to dynamic claims solutions

Claims processing has four high-level modules: First Notice of Loss (FNOL), Holding, Finance and Claim Closure. The FNOL process consists of sub-level services that can be classified as individual application program (API) services for internal and external systems and listed as unbundled sub-components. In an assembly business model, these disjointed components can be reassembled to form dynamic modules.

View the big picture

4. Straightforward Processing (STP) on Claims – from time-consuming review processes to automated API-led approvals

Straight-Through Processing (STP) claims refer to high-volume, low-value claims that can be paid quickly without a detailed adjudication process. In this case, different APIs are used for the following processes: from the basis of taking a claim; policy search and return; attaching a request invoice by pushing invoices with a vehicle or request number automatically; to ensure the inclusion of certain information on the invoice; and to see if the invoice amount is below the STP limit (say $350) defined by the insurance company. Based on the results of all these API processes, claim payments can be automatically approved and the amount paid to the insured immediately. These can be used for ‘glasses only’ car claims, as well as less expensive medical injuries.

View the big picture

5. Simplifying the Monolith – from large legacy infrastructure to a flexible, agile approach

In current discussions with clients, we are recommending the simplification of monolith architectures in order to effectively implement a modular architecture. This means the process of gradually dismantling the existing infrastructure and rebuilding it in a more efficient way. Monolith simplification helps reduce risk when a client has an active monolith system that supports the business and continues to evolve.

Once we determine that a scalable design can be implemented, we approach it in three stages – understand the challenge, assess the required action, and implement the solution. Following this first approach, another component checklist can be constructed to isolate the monolith experience.

Contact him to find out how he can be used to guide and grow your Total Enterprise Reinvention insurance business.

Designation Helps New Producers Build Confidence, Credibility, and Early Success.")